One of the big problems we try to solve in financial planning is... how much money do you need in your life?

We talk about expenses, potential costs, investments, savings but one big piece of the puzzle is missing. When will you die?

Tomorrow? Or at age104?

It’s a pretty major factor that we have no clue about.

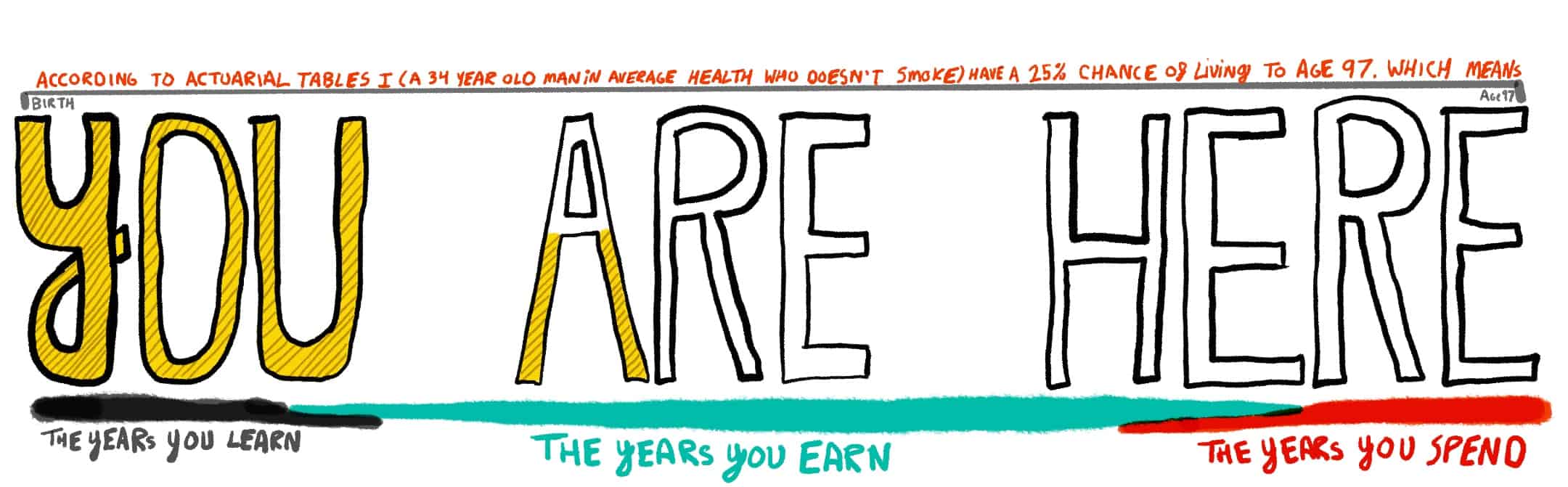

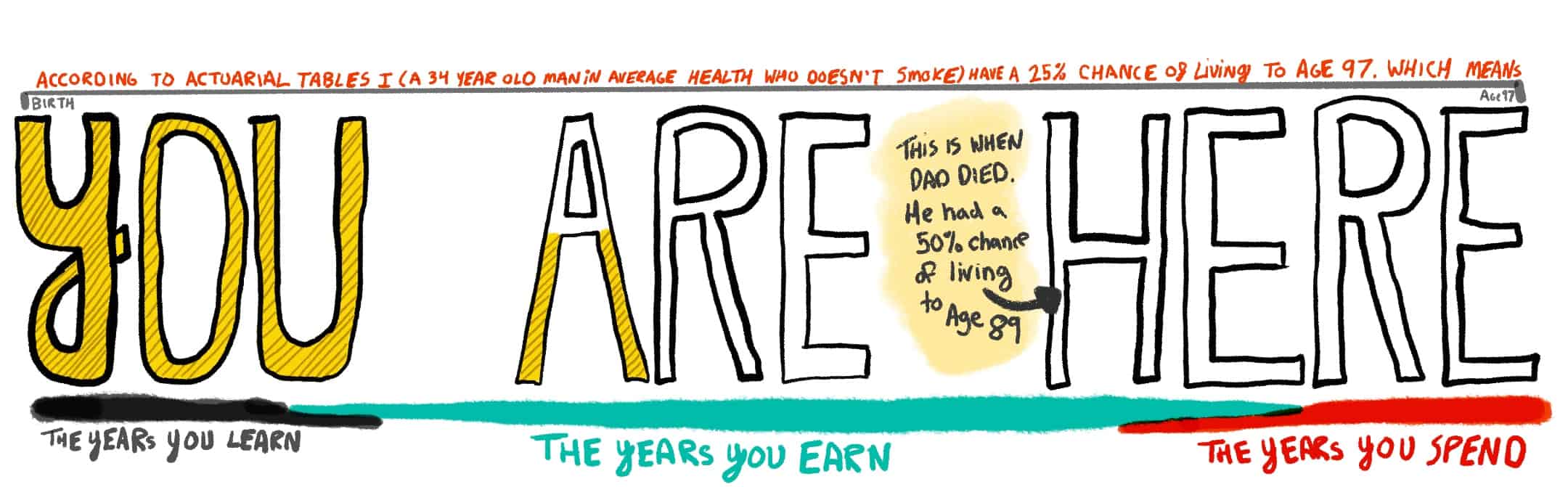

We “solve” that problem by making a reasonable guess. By looking at actuarial tables we say - what’s the % chance that you at age ____ will live to age _____.

The financial planning standards are to plan until you have a 25% chance of living past a certain age.

Isn’t that simple? Not really.

The hard question at the core of this problem is not the math of “how much do I need to live to 95”. That can be estimated with a few formulas and a financial calculator.

The hard question is how do we balance your need to live and enjoy your life now with the fear of running out of money in the future.

My dad died at age 72. His chart said he should be planning for another 20 years.

I’m so glad he didn’t. I’m so glad he focused more on enjoying his life than worrying about age 95.

That’s easy for me to say now, because I know the answer to the when--will-he-die question. And his death has called into question the true complexity at the heart of retirement planning.

It must be balanced. Some of you are excellent, intentional, in-the-moment spenders. Some of you are great in-the-future savers. But you need to talk. Learn from each other. We need both of these skills to have a shot at the right balance.

This is really hard, but it’s an area in which planning can really help. Not because it'll show you what will happen, clearly we have no idea. But what it can do is guide you through the process of fully considering what you want, both now and later. What do you want your impact to be? Where do you want resources to go after you’re gone? How do you want to live now, and how can you build meaningful spending towards those values now, while balancing potential futures?

Never let anyone convince you that saving is all there is to solving your later life planning. It’s only a piece of the puzzle.