Your number is what your life costs.

Knowing how much YOUR life costs, is a really important piece of information, especially for those of us living on variable income.

You know that fantastic feeling. You’ve just been cut a check for 4,000 dollars. Let the caviar RAAAIIIINNNN!!!!

Or wait. I’m not working for the next couple of months. I wonder how much of this cheque I’m going to need…

So you do some quick calculations, add up your rent, what you imagine you spend on food, a phone bill… oh right, and internet…..um.. There’s probably lots left. I’m just gonna make it rain a little bit, then go hot air ballooning with my friends… okay????

*Sigh*

This is why you need to know your number!!!

So how do you figure out ‘your number’?

First of all, let me clarify… when I’m talking about what your life costs, I am not talking about what your business costs. I don’t know your business, but what I do know is that as a freelancer … business is anything but constant. Your business could eat up all the money you send at it; It’s where all kinds of crazy variable costs and expenses might be lurking.

We’re looking for constant, reliable things. Things we can control. Things that make the freelancer lifestyle feel a little less out of our hands. That constancy is found in your personal costs.

Remember here, before you write me off for looking at this too simplistically, that the primary function of your business is to provide you, the individual human, with the resources to live the life you’ve chosen. Knowing what your number is, is essential information for the business part of you. It lets that side of you know the minimum income it needs to bring in to support YOU!!!

Okay… We can get your number by laying down your constant monthly costs. Remember we’re trying to build a number that doesn’t change all over the place. A nice solid number that we can take home to meet the parents.

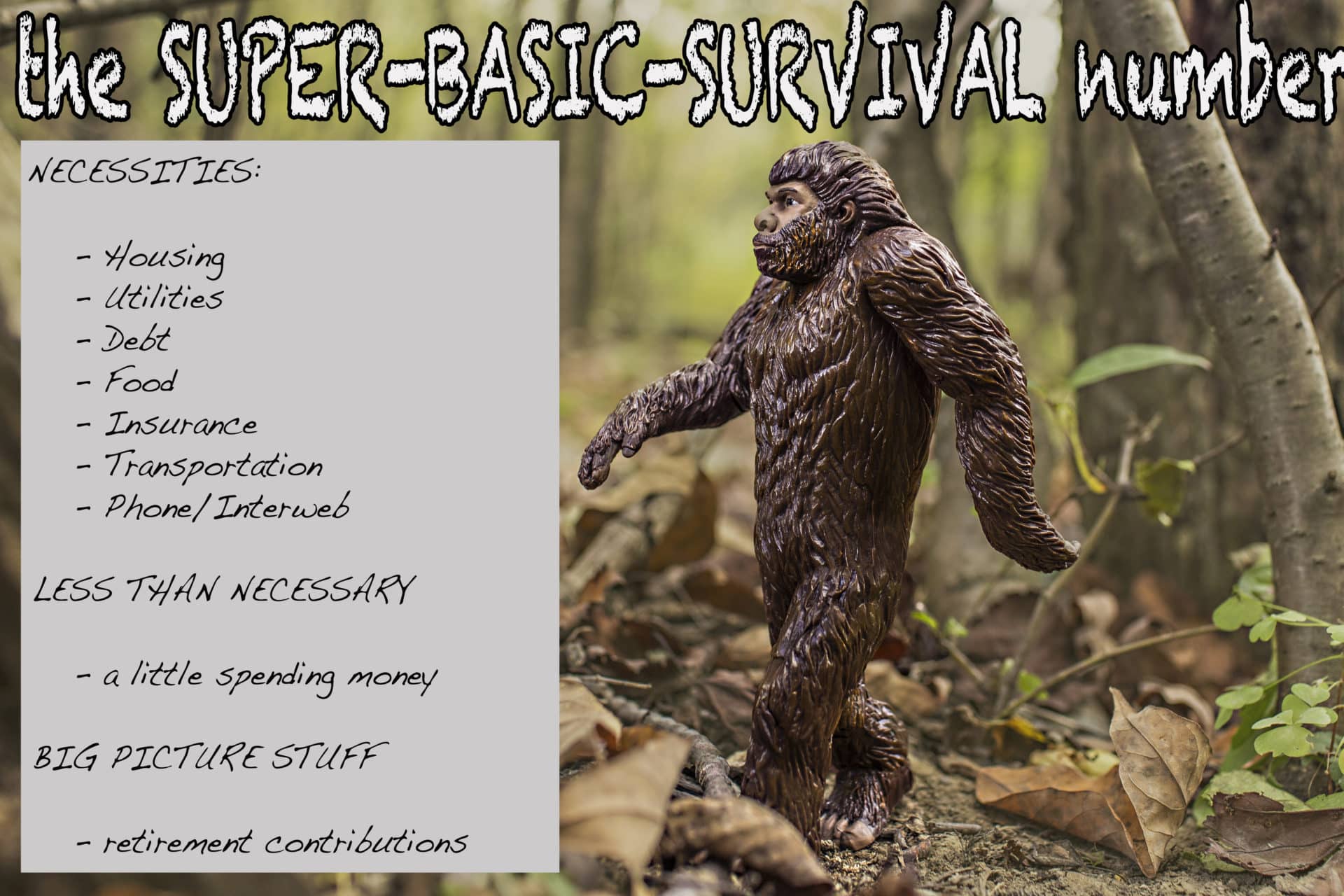

First the necessities:

These are the bills you HAVE to pay or one of the following will happen:

1. You will die

2. A man will come and find you with a bat and break you (or your credit score)

Housing (Rent, mortgage, condo fees)

Utilities (Cause you’re gonna want heat… especially if you live in Canada. Also other things you need like water.)

Food (You gots to eat. Figuring out how much you need for food may take a little time. This food category is really for the kind of food you buy and make at home… not for fancy food … which is what I now call eating out)

Debt payments (You gots to pay… remember the guy with the bat…)

Insurance (Life, health, dental … etc)

The next few I put in the necessities category even though they don’t really fit in my two rules. Mock if you’d like. I consider these all to be definite necessities:

Phone (cell and/or land)

Internet (I know it’s a utility, but it deserves its own category… and also… you do need it.)

Transportation (car, transit, bike)

The less than necessary:

Your life is more than a place to live, some ramen noodles and some internet.

Fancy Food (Cause that’s what we’re calling ‘going to restaurants’ today.)

Entertainment (Fun stuff you like to do, and also Netflix… the thing that keeps you from going out and doing fun stuff.)

Birthdays/Christmas (I know Christmas doesn’t happen every month, but it does happen every year… part of my number is putting away a little bit every month so it doesn’t kick me in the butt.)

Clothing (People like clothes, right….?)

Spending Money (Cause sometimes you just need an Archie comic.)

The big picture stuff:

Whether you’re doing it or not, it’s good to start thinking long term, and be tucking some money away every month to two things…

An emergency fund (it’s for emergencies)

Retirement (For those days when watching 12 episodes of House of Cards will be your reality… even more than now…)

Now, take the amount that you spend on those categories every month and add it all together.

That my friends is your (current) number.

Now the personal finance purists are freaking out. I included a bunch of stuff (most of the ‘less than necessary’ items) that shouldn’t be monthly costs.

But here at Rags to Reasonable, I’m way more interested in your actual number than the one that looks good on paper, and doesn’t actually match the life you’re living at all.

It’s your number. You get to decide what your ‘basic’ life looks like. Some people would look at the life I live and call it super fancy, others would say it’s barely living. The most important thing is that you can actually afford it. If you just did the math and ‘your number’ is way more than you normally bring in in a month… well… that may be a problem. You may have to adjust some of those constant expenses, play around, see what balance you can live with. But there’s also the fact that you’re going to be going through stages of life when you make money, and stages when you’re not making any.

And so… for all of the different stages (or at least three of them) of your variable-income-earner-crazy-life… here are a few different number options that you should have in your tool belt.

You don’t have a lot of money. In fact, it feels a whole lot like no money. What is the least amount of money that you can live on (and still achieve a base level of physical, spiritual, and mental health)?

Finding the wiggle room:

House, utilities, insurance and debt, probably not a lot of wiggle room there. But Food costs can go down. Play around with the least you can live on and still be healthy. Transportation has some possible wiggle room. If you have a car payment… that’s a set cost. But if you live somewhere where you can walk (or bike!!!) you can really cut the amount you spend on transportation. Phone/internet is up to you. I consider these must haves in my basic budget. There are others who wouldn’t. You can also think about cutting services for certain months or switching to a more basic plan.

As for the less than necessaries… this is the category that gets a pretty big cut in super basic land. But even when I’m living on very little, I always put aside a few bucks a month for spending money. You need some kind of fun. If there’s no room for it in your number you’re just a ticking time bomb for a giant credit card ‘spree’ of some kind.

The big picture stuff stays a part of my super basic number… No matter how little I’m making, ‘my number’ always includes the big picture stuff. Of course if you’re really struggling to eat and make rent, this one can get tossed out, but when you’re building ‘your base number’ I would really recommend including some kind of thought to the future (unless you’re cool working until you’re 93… in that case… party on!!)

It’s tough to live in survival mode for a long time. It’s stressful, and though most people are capable of it, it does start to wear. As important as it is to know the bare minimum that you can live on, the LEAN-MEAN number is built for streamlined comfort.

Don’t get me wrong… it’s a no frills life, one that I believe is built for the small business owner in start-up mode. Most of your resources are funneled into growing your business… but your personal life has a few perks that make life a little more pleasurable in the meantime. Remember a healthy artist is a more productive artist!

The changes: On top of the SUPER BASIC model, I add back in some of those ‘less than necessaries’ discussed above. I don’t allot a lot of money towards any of them, but I give myself permission to go out for the odd ‘fancy food’ (ya… it’s annoying to me too… but I’m sticking with it), and have a little fun.

Personally, I’m partial to the ‘fancy food’ and entertainment categories… but if you’re more of a shopping person, put a little money there. Remember this one is built for distance, so it’s got to be a little comfortable.

The bulk of my money is still going towards my necessities, and the big picture stuff, but there’s just a little bit of breathing room.

If you’re making good money, there’s no reason to be living in survival mode, or even survival PLUS. I had coffee with a fellow artist a few weeks ago whose monthly number was almost 5 times my number, but we’re in really different places. He’s still doing all the same things I’m doing, but a lot of his costs are higher (housing, and retirement contributions), his income is also a lot higher than mine… so it all balances out.

I don’t have a template for a living-the-life number. I haven’t quite gotten to that point yet. So above, I added a few luxuries I wish I could be contributing to constantly… like a travel fund and some new clothes… But you get the idea.

Whether it’s making a budget, figuring out how to pay yourself a salary, or trying to see how long a big pay cheque will last you, knowing your number is just not optional.

Knowing what your life costs is essential. For some people that SUPER BASIC life that I outlined is just not an option. That’s totally fine. But there are some big life choices to be made because of that.

For most artists I know, there have been times of living in that SUPER BASIC lifestyle mode. Deliberately making choices about what you can and can’t live without can help you figure out how much money you NEED coming in to support those choices, and see how that matches up with the realities of your career.

Maybe that means diversifying your income, or taking a few more jobs in a year (whether or not they seem ‘artistically stimulating’).

And once you figure out where those sweet spots are, for both the SUPER BASIC, and the longer term strategy… it becomes another great constant in the fields of things that are out of your control.

And that’s what I’m all about here at Rags to Reasonable.

Ignoring all the crazy, and focusing on those few things that you can control.

In this case.

Knowing. Your. Number.