Whenever people start throwing around financial terms like inflation, it’s easy to tune out immediately. But, aside from being crazy interesting, inflation is one of those big financial forces that affects you every day. It’s basically like gravity… yet another thing that’s keeping you from the miracle of flight….

Whenever people start throwing around financial terms like inflation, it’s easy to tune out immediately. But, aside from being crazy interesting, inflation is one of those big financial forces that affects you every day. It’s basically like gravity… yet another thing that’s keeping you from the miracle of flight….

Ugh. I wanna fly so bad.

But seriously… understanding a little bit about inflation is actually super important, especially for those of us who are trying to stretch every dollar.

I’d even go so far as to say that ignoring inflation could end up costing you a ton of money in the long run.

What is inflation?

A few thousand years ago people got sick of carrying goats around to trade, so they started to use a more portable monetary system.

Money. Gold Coins, and paper pictures. It’s become a big crazy constant.

No matter what you do you have to deal with money.

But in fact, money is way less ‘constant’ than you’d think. Sure, a dollar is worth ten dimes and it always will be (well, until we discontinue the dime), but the VALUE that dollar represents has changed hugely over time.

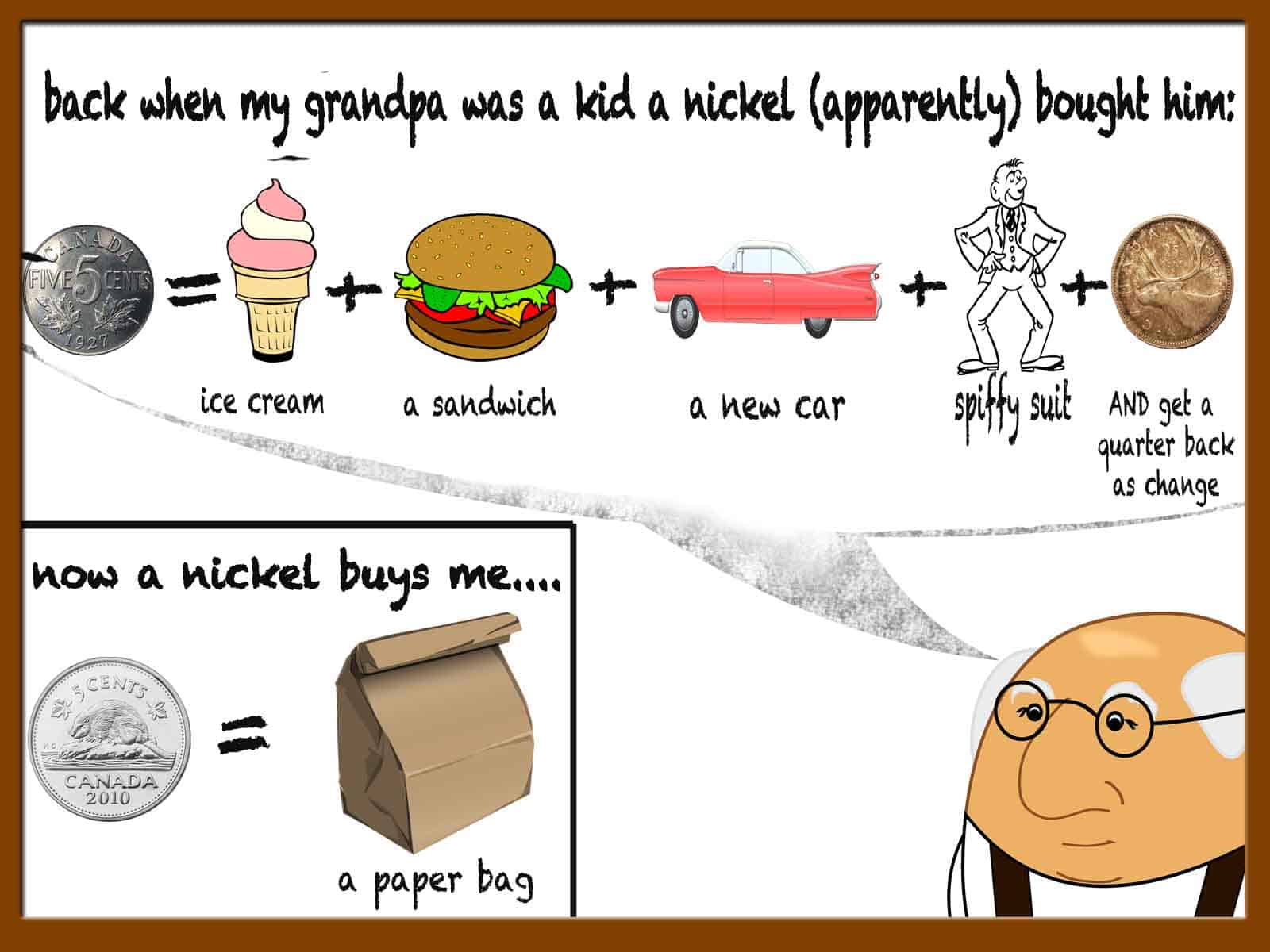

You’ve heard it from your grandpa.

“In my day a nickel would buy you…..”

That’s all because of inflation.

That’s all because of inflation.

Inflation is just the name we give to the general increase in prices over time.

Simple.

How do we keep track of inflation?

Not all price increases count as inflation. Sometimes the cost of something just spikes for one reason or another (mainly I blame Apple, and their pretty pretty things).

But Canada has a way to tell the difference.

Every year Statistics Canada takes a look at something called the Consumer Price Index, which is a not-so-fun name for a giant basket of goods that represents what the average Canadian consumes annually.

Oooo! A giant basket? Of goods?? Colour me intrigued….

This is a fascinating concept to me. Wouldn’t it be fun to hit COSTCO up for the Only-Shop-Once-a-Year-Big-Basket-of-Canada?! What’s even in there? What do they think the average consumer needs? What’s basket worthy? Did Timmy’s piano lessons make the cut?

Turns out the basket is full of exactly what you would expect. Food. Shelter. Household products. It tracks the price of frozen french fried potatoes, soft drinks (more specifically the lemon-lime type) and, never fear, almost 5% dedicated to the heart of any artistic profession – alcohol and tobacco!….*tear*… they thought of us, guys….

Every year they take these prices and compare them to the previous year, figuring out how much more expensive things have gotten. Of course it’s all much more complicated than that… but in the end they get to a nice clean percentage point.

Here in Canada we’ve averaged around 2.4% inflation for the last 25 or so years. The government actually works really hard to keep it in-between 1 and 3 percent at all times, and they’re pretty dang good at that.

2.4%…. that doesn’t seem like so much… right?

But here’s a super important finance lesson.

Little numbers make a huge difference over time.

Just a few percent here and there, when it keeps happening over years and years, starts making a real difference.

And here we come to the reason inflation matters to you.

Inflation is stealing your money.

And it’s doing it with evil-genius-like style. It doesn’t apply a fee to your bank accounts, the numbers never change, but the VALUE goes down (or what finance nerds call ’purchasing power’). Which means, what you can buy with that money… gets to be less and less every year.

Don’t believe me?

Remember the year 2000? Y2K… all that fun stuff? If you would have stuck 1000 dollars under your mattress (to save it from the the Y2K bug… of course) and pulled it out today… you would still have 1000 bucks.

BUT.

That 1000 bucks back in 2000, would have had 33% more purchasing power than now. Or… to put it another way, something that cost you 1000 bucks in 2000 would now cost you more than 1300.

And that’s just 1000 bucks, in 15 years.

From the Bank of Canada’s inflation calculator… a fun (and sometimes scary) thing to play with.

Little percents make big differences.

Every year your money is worth less.

So… what can you do? Put that money to work!!

It seems kind of inevitable, inflation’s slow march. It seems like the only thing to do is to just try to make more money. OR you can figure out how to put your current money to work!

First of all, it’s important to note that inflation isn’t that big a deal for the money you’re planning to spend in the next few years. Ya, milk may go up a few cents, but generally, you’re going to be fine.

The thing that inflation really hits hard is your long term savings.

Dr. Inflation???

It’s that money that you have sitting on the side in a generic savings account. That money that you know you should do ‘something’ with, but you don’t quite know what.

It feels like it’s safe. But anything that is guaranteed safe is still open to the meddlings of Dr. Inflation. (Possible villain name? Open to suggestions, people!)

And even if you’re being paid interest in that account, the typical banks aren’t paying enough interest to cover THE INFLATRON (I think that one’s better).

So, in this case, the price you’re paying for safety is the slow erosion of your cash.

This is one of the big arguments for learning the basics of investing.

By putting your money to work, even in a fairly low risk way, you can make sure that at the very minimum your money is holding its value for the years to come.

or THE INFLATRON!!!!

Investing isn’t just for people who want to get rich. It’s for people who want to make sure that the money they’ve worked so hard for, scrimped and saved, still has its true value whenever they need it.

So maybe it’s time to start digging around a little and giving the ‘investing’ thing another try. Here at R2R we’re gonna talk lots about investing: the different options, and the right questions to ask to find an investing style that feels comfortable to you.

But in the meantime, check out where you’re keeping your long term savings… and keep a wary eye out for …

INFLAMMATION!

…Ugh… sorry….

Another option is putting a bit of one’s savings in gold or silver . Not so much as an investment but as a hedge against inflation. Gold and silver coin’s are easier to get than one might think, you just need a safe place to store them.

Hey Rolf,

You’re totally right. Some folks swear by gold/silver as an inflation hedge, but it’s really all about the time frame you’re talking about. Gold and silver run on their own cycle, and can bite you.

I was reading a piece the other day that insisted that over a long time frame the best inflation hedge is still stocks or real estate.

What do you think? Have you had good luck with gold? Maybe I should take a trip to my local pawn shop….

Well a friend and I where chatting this week on our investments and we have taen a worse hit than “inflammation” this past month. Called “extreme deflation”. Especially if you are in Canada. The plunging “petro dollar” – soaring U.S. $ – has costed us much more then the so called inflation example you have shared. I would have been happy with the 33% loss.

Well.. I doubt anyone promised you that your money was safe when you invested in the oil fields, or the dollar. Over the long term, these investments might rebound… but when you’re talking about inflation… it’s a different story.

It chips away at ‘safe’ money, and leaves no chance for return.

Investing isn’t a simple prospect, and of course there are risks, but when matched against a guaranteed longterm loss it has to be explored.