It’s hard to work in December, so I’m throwing in the towel on starting new projects. What I’m going to do instead is talk a little bit about the last year.

One of the coolest things about budgeting consistently is that at the end of the year you can take a look back at how you spent your money. It’s like a financial scrapbook, and if you’re budgeting in YNAB they even make the reports pretty and shaped like pies… so, double plus!!

So I’m going to break it down for you guys.. where my money went and how I feel about that.. but first, here are a few provisos (#fancyword).

- I’m not going to use exact figures. This isn’t just because I’m not entirely sure how I feel about sharing my numbers online yet (it’s kind of a weird thing to think about), but because I think that exact numbers can be misleading.

I can spend 3000 dollars a month on rent and have that be a completely reasonable expense if I’m making six figures, but that sounds insane to someone who’s making just above the poverty line. A number means something different to everyone.

Instead, I’m going to use percentages of total income. That shows where the big chunks are going, and where my financial priorities are. - This is not a clear representation of all my spending. I’m going to start with just my personal side, so there’s no business stuff in here. One of the things that I separate between business and pleasure is food costs. When I’m on a gig it’s a business cost, when I’m not it’s usually a personal cost. So my food costs on the personal side of my record keeping are way lower than they actually are in total, because sometimes food is a business cost.

There are a few things like that… I’m not trying to trick you, or show false date… it’s just the way I order things. - This is just my spending. Not my income. Seems like they should be related, and they are, but a bunch of my spending (particularly the dental costs) came from previous savings… not from income I made in 2015. These charts just talk about how I spent all the money that I spent this year.

What I’m trying to show is how I order my spending, and what kinds of things I’ve chosen to invest in (ya… it all counts as investing).

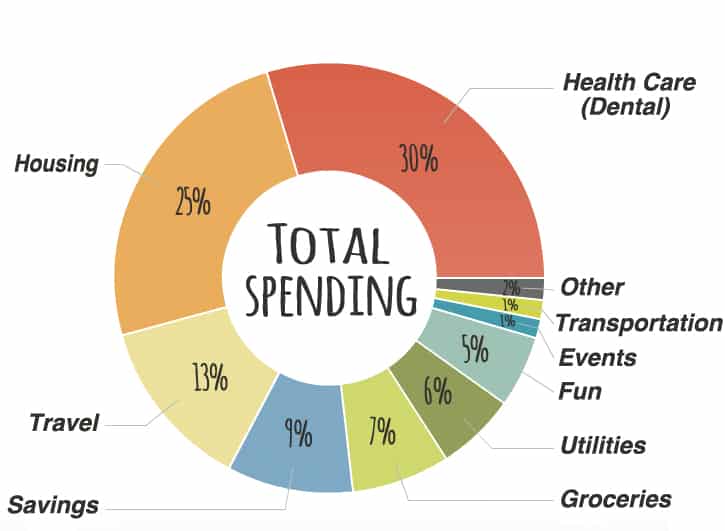

How the non-business me spent his money in 2015

There it is, in all its splendour. A year boiled down into unarguable facts.

You see, I can talk as much as I want about the things that I care about, the things that I want in my life, but a budget report is black and white (or in this case, multiple colours).

So let’s break it down even further, and stick to the facts. What did I spend my money on?

Housing: You gotta live somewhere…

Housing is 100% rent, and accounted for 25% of the money that I spent in 2015.

Housing is 100% rent, and accounted for 25% of the money that I spent in 2015.

I live in a three bedroom apartment on the second and third floor of a house in Toronto. I live with my girlfriend and another roommate, which keeps costs down.

The official financial planning rule of thumb when it comes to how much you should be spending on housing is ‘no more than 32% of your income’. Obviously, that can be a ridiculous goal if you have a low income and have to live in a big city like Toronto or New York. But if you’re curious, it’s a place to start.

Housing is always a huge cost, but it’s one that most of us have.

Not included in this: all of my housing for gigs and business trips. It’s only my personal home (although I do use part of that home for my business).

Travel: When I do it… it’s not a luxury

13% of my spending was on travel. And remember, that’s not business travel… that’s all personal. It may seem like I’m living large and fancy free but I don’t see it that way.

The lion’s share of my travel money went to my long distance fund . My girlfriend and I are apart for about half the year, and since we generally want to see each other during that time we set up a way to put aside money every month so that we are both sharing the cost, and investing in our relationship.

You can read more about how it works (and if you’re in an LDR, how to set one up for yourself) HERE!

The rest is from once-a-year expenses. I only ended up heading home once this year at Christmas, and the rest is from one of my best friend’s bachelor party when I traveled back home and we rented a cabin. It was a pretty great weekend.

The reason I don’t think of this travel as a luxury is that it’s not travel for travel’s sake. These days I’m not spending on vacations to a beach (not that there’s anything wrong with that… it’s just harder to argue that it’s not luxurious), I’m spending money on the relationships that are important in my life: my partner, my family, and my closest friends. In my books that’s a necessity.

Non-consensual savings (is that the same as forced savings?)

Savings are a part of my monthly salary, and are automatically taken out of my account. You can set up ‘forced savings’ programs with your bank, so that they take a certain amount every month and put it in a savings or investment account.

Savings are a part of my monthly salary, and are automatically taken out of my account. You can set up ‘forced savings’ programs with your bank, so that they take a certain amount every month and put it in a savings or investment account.

At some point I’ll get around to talking to you guys about how I invest, but suffice it to say that I put almost all of my money into a TFSA instead of using my RRSP (except apparently for 2%… I don’t really remember doing that). The decision to do that needs a longer post all to itself. If you have questions about it that need to be answered right now… send me a note.

These savings aren’t for now… or even 5 years from now. Barring some sort of catastrophe they’ll sit around there for the next 30 years harnessing the magical powers of compound interest.

Chickpeas and rice… rinse… repeat…

This category couldn’t be less interesting… mainly because the big questions when it comes to groceries don’t have to do with percentages.

How much do I actually spend on food?

How much do I actually spend on food?

It varies. Not only does it vary, but this chart is one of the parts of this report that isn’t all that accurate. Like I mentioned above, I split food in my records depending on whether I’m away on a gig, or whether I’m at home.

In months when I have some extra breathing room my grocery costs can by as high as 350 dollars, and in lean months they can be as low as 200 dollars (which is really hard for me).

LOWER YOUR GROCERY BILL WITH A SIMPLE PLAN… A MEAL PLAN. FREE WEEKLY TEMPLATE HERE!

I also feel the need to say that spend more than 1% of this budget on my hygiene costs! I only recently made it a special category in my records and I don’t always enter it (bad finance blogger). I buy my shampoo at the grocery store so it all gets lumped together sometimes. #notthatdirty

My cell phone is the bane of my budget

I think my secret shame is how much I spend every month on my cell phone. I know that it’s expensive in Canada, but I feel like I should be able to find a way to make it cheaper. I just chicken out every time I consider cutting my data.

I think my secret shame is how much I spend every month on my cell phone. I know that it’s expensive in Canada, but I feel like I should be able to find a way to make it cheaper. I just chicken out every time I consider cutting my data.

So that’s how I end up spending a huge portion of this Utilities section on my phone.

Internet doesn’t end up costing much when you split it with a few roommates.

Now, bank fees. I have talked a lot about how great no fee banking is, and that’s true. But I still hold an account with TD which charges me some fees. I do it for a few reasons: I like having separate accounts for my business and my personal, and I have investments with TD that I like. So I stay… and because I stay, I also pay. #poetpoints

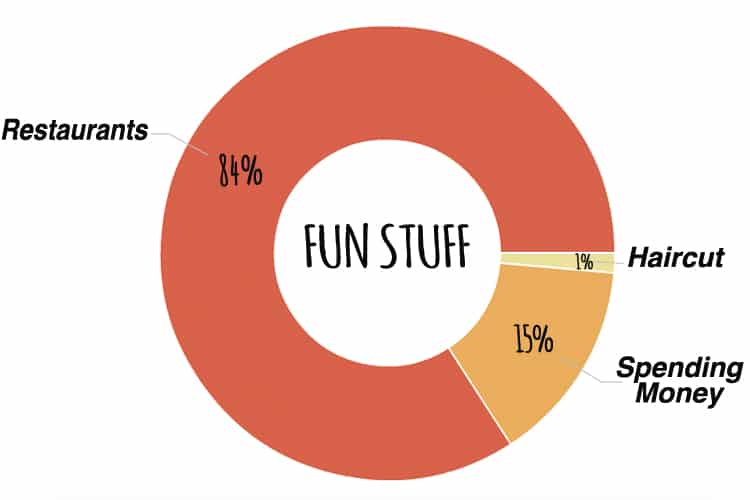

Girls just want to have fun (and since genders are equal….so do boys?)

By looking at this section you might come to the conclusion that in my mind, fun = food.

You would be correct.

You would be correct.

Why do I have restaurants here in the ‘fun’ section, and not in some kind of ‘food’ category?

Because I like to remind myself that restaurants are a luxury. I don’t have to go to them. I do it for a treat, and when I’m lazy (which is all too often). And they’re fun.

Not included: all the times restaurants aren’t just ‘fun’… which is when they’re for business. That’s all in my business budget and spending.

Another section of the pie is that tiny portion for haircut… again with the embarrassingly small number dedicated to personal grooming (hello ladies), which I will justify by saying… I moved haircuts to another area in my budget early in the year, and for some reason I guess I didn’t get them all written down! It’s a glitch, but it’s a glitch that I’ll stand by. The data doesn’t lie: I think haircuts are fun, so much fun that I only get one a year (#jokehashtagincasesomeonethinksimserious).

Spending money is an absolute must in the budget of Chris. No matter how little money I’m budgeting with I always stick in a section for random spending. It means I can grab a magazine or some lip smackers just for me. It doesn’t have to be much, but in my mind, it has to be there.

Christmas is coming…

It’s December. I’ve managed to limp into the last few Decembers with not a lot of money, which sucks because Christmas is expensive.

It’s December. I’ve managed to limp into the last few Decembers with not a lot of money, which sucks because Christmas is expensive.

I save a few bucks for Christmas every month of the year. That way when I get there… it’s fun! I do the same for birthdays and date nights. By throwing 30 bucks into my ‘events’ category every month it keeps stuff like birthdays and other holidays low stress, because instead of trying to scrape up the cash to buy little Johnny a pair of skates… it’s already there waiting to be spent.

It’s all well and good to say that you’re going to cut back on presents, but life events cost money. It’s part of the cost of having family and friends. Instead of lying to myself about how I’m going to cut costs, I’m steering into the skid and making sure there’s money there when I need it.

Vroom vroom vrooooooomm

Transportation makes up a tiny fraction of my spending for a few reasons.

- I bike everywhere when I’m home (even in the winter) so I only need to take transit when it really storms.

- I don’t own a car. Cars are expensive, but also necessary if you don’t live downtown in a major city. So that’s a luxury for me!

- I steal coins from everywhere possible whenever I need to take the bus… that money often doesn’t get recorded in my budget. So… I’m basically cheating.

- I can be pretty introverted, especially in the winter. The best way to save money is never to leave your neighbourhood.

The spending here is pretty clear. A little for bike maintenance (although I should really be spending more… my bike needs a tune up), a little more for transit, and the odd taxi to fill out the list.

I have some fuel costs even though I don’t own a car. It comes from the times that I borrow a car and fill it up, or chip in for gas when someone else drives.

How I paid for my dentist’s vacation

I’ve talked a lot about my dental woes this year. I won’t go into them again, but trying to fix my teeth has been the biggest cost of my year.

I’ve talked a lot about my dental woes this year. I won’t go into them again, but trying to fix my teeth has been the biggest cost of my year.

During 2015 I had:

- 6 root canals

- over 20 fillings

- 20 hours spent in a dental chair

- so many freezing needles

- achieved a decay free mouth (except for my wisdom teeth, which still need to be pulled).

There’s more work to do, but I don’t feel bad about spending that much on my teeth. They needed to be fixed, and I’m fixing them. That’s the end of that.

Where did the money come from?

Part of the initial payments came out of savings from the last few years, the rest came from scrimping and saving. I pay myself a fixed income every month from my business, and so I needed to find the extra money in that to pay my dental bills. I borrowed some money during the year to get the work done, and then I paid it back by November. It was hard, it’ll continue to be hard, but that’s how debt repayment works (and yes… what I’m dealing with is debt… dental debt).

All the other stuff

YNAB won’t make me a chart for the last few categories, so I’ll have to do it without the flair. There are three categories here:

- Giving

- Clothing

- Business Float

Giving refers to charitable donations, which I’ve been trying to step up in December by giving at least 5 dollars every day. It’s been fun, and reminded me how good it feels to put your money at work in the world.

Clothing. I don’t spend much on clothes. Sometimes I wish I did because most of my clothes have holes in them… which isn’t great. But the facts are there. Expect that category to be higher in 2016.

My business float is a really useful budget category. It comes in to play all the times I end up using my personal money to cover a business cost. It happens, and it can be a bit of nightmare to record properly. So I keep a little money on hand to cover those business costs, and then my business account pays me back. I’ll write more about how that works in a later post, but if you have questions feel free to send me a note.

2015 in a financial nutshell

It’s a pretty crazy way to look back at the year.. all the little choices that I made, all the little successes and lapses displayed in a few colourful pie charts.

It’s actually been fun to look back and spend some time with my records over the last week. I feel like the way I’m spending my money these days is pretty in line with how I want to be spending it… and that feels pretty good.

What about you? How did you spend your money this year? Is it in line with what you wanted or did you have to put out a lot of financial fires? Why not share some of your 2015 money memories in the comments starting with the following sentence…

2015 was the financial year of the __________

(for me it was the year of the tooth)

I see you don’t monetize your page, don’t waste your traffic,

you can earn extra cash every month. You can use the best

adsense alternative for any type of website (they

approve all websites), for more details simply search in gooogle:

boorfe’s tips monetize your website