If you’ve been in Canada over the last month you’ve probably seen a ton of ads and ‘reminders’ (they’re also ads) to put money into your RRSP.

DO IT! PUT MONEY IN IT!

DID YOU KNOW THAT MOST PEOPLE DON’T?? DON’T BE MOST PEOPLE! JUST PUT THE MONEY IN.

Ughhhhhhh.

That’s because we’ve just come to the end of what wonderful finance nerds the country over call ‘RRSP season’. It’s the time of year when lots of people are making contributions, topping up accounts, and looking to get their tax efficiencies in order.

But most of us… we’re just trying to get through another Canadian winter.

Actually, I think a lot of us just don’t really understand what an RRSP is… yet.

I sure didn’t.

I thought I did… but if I’d been asked to explain it… it would have probably sounded like this…

“Oh ya, an RRSP… um.. You just get one, and it’s for retirement… and you should really have one… but I don’t have one… I guess I should do that.”

I mean… why would you even need to read the rest of this post?? I think that definition is pretty clear.

But in case it’s not, today we’re going to break it down, and I mean really break it down. We’re going to talk about what an RRSP actually is, how it works, and whether it’s the right tool for YOU and your life.

Because let’s be honest… RRSP’s are great, they’re an amazing and pretty powerful tool for long term savings, but after I learned how they worked… I stopped contributing to mine.

It wasn’t the best tool for me, and it might not be the best tool for you either!

RRSP’s 101: Why should I even care about this?

Before we talk about those 4 letters and what they mean, let’s dig a little deeper. This conversation is all about ‘saving’…

What’s the point of saving?

Seems like a simple question, but the truth is a whole lot of people don’t really see a point in saving. I could go on about the awesomeness of ‘delayed gratification’, but for now… let’s not worry about the small reasons to save. Today we’re not talking about saving for a vacation, or a car. We’re tackling the big daddy of reasons to save:

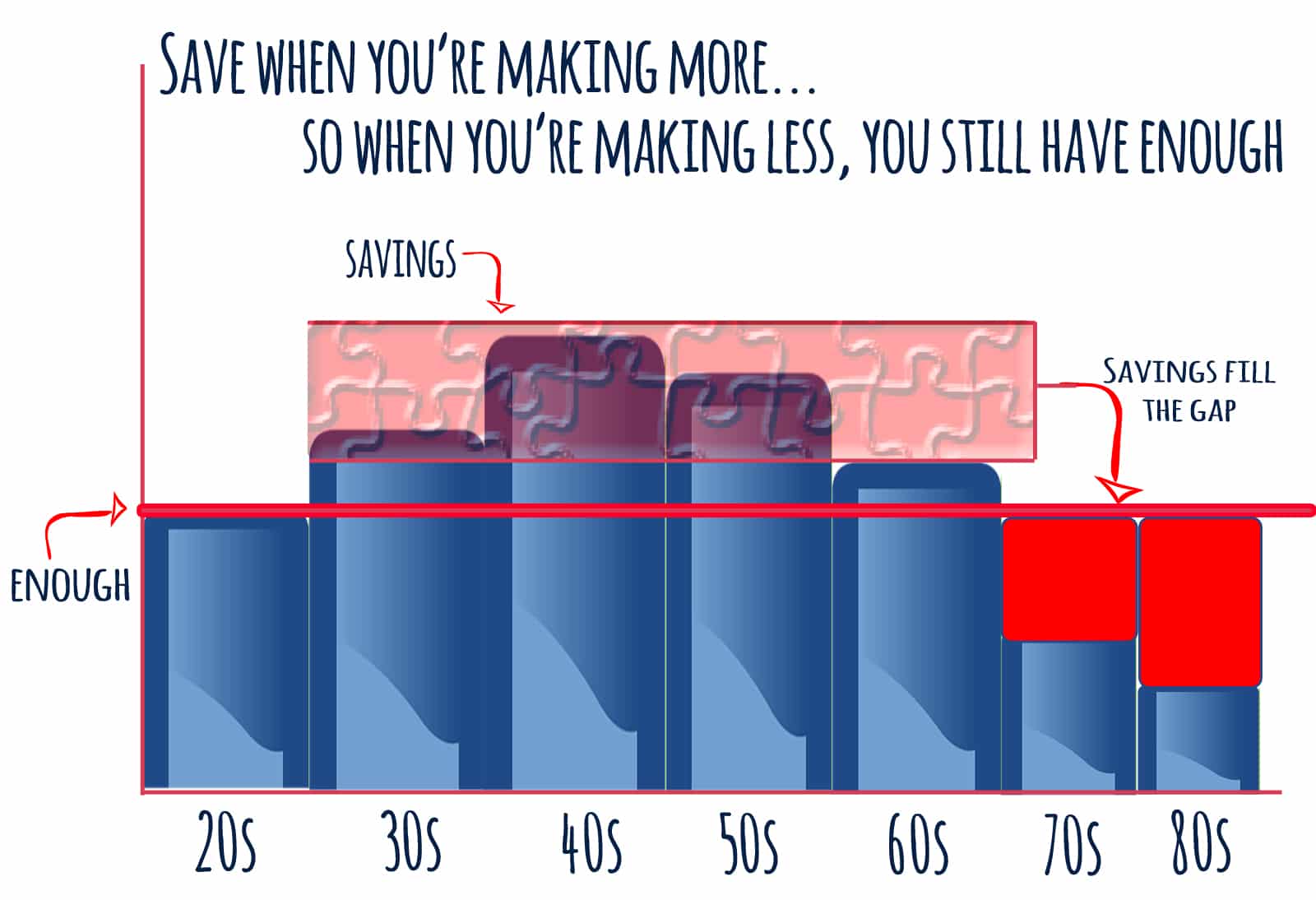

When you get older you’re going to need some money… and you might not be able to work for it.

I’m going to admit something. I don’t really like the word ‘retirement’. I honestly think it’s a word that’s going to disappear from conversations over the next 30 years. But that’s all semantics. Whether you like it or not you will probably reach a point in your life where you can’t do the work that you used to be able to do, and therefore will make less money. That’s the basic core reason why you need to save for retirement.

When you’re making more money… save some of the extra for the time of your life when you won’t be able to make as much.

I get that this chart is an oversimplification… #chill. The point is just to visualize what people mean when they talk about ‘retirement savings’. It’s basically about transferring ‘extra’ money when you’re younger up to the years when you won’t be able to earn as much.

But what if you’re not making much right now? Like when you’re a freelancer in the first years of starting a business… should you be worrying about saving for retirement then?

Why it pays to start early…

No one wants to talk about retirement when they’re young. It feels morbid and weird.

But starting early is the best way to turn a little money into enough money. Enough money to not ‘have to’ work when you’re older.

How? Through the magic of compound interest.

I won’t go into it too much (you can read my Harry Potter themed article above if you want to get the nitty gritties on why compound interest is better than a butterbeer on a cold day), but here’s a simple formula that explains everything.

Money + time + the right tool = way more money than you started with

That’s the basic idea that all the financial types are working with when they start harping on young people to save early. It’s the positive spin on why they create ads to try to pressure you into contributing to an RRSP.

They mean well, and they’re 100 percent right about the saving early thing.

If you want to see it in a more official chart form… check out THIS chart, or THIS one (WARNING: none of them talk about Harry Potter).

Saving early will help you out hugely later in your life.

But here’s the thing, there are also a billion other demands on your money when you’re young. You want to go to school, and start a career, and build a family, and travel, and maybe buy some sort of dwelling.

You get to decide where to spend your money, but I’m going to tell you right out of the gate an RRSP is not a tool for a travel fund, or to support your business. It’s for retirement. It can be used for a few other really specific purposes (which we’ll discuss), but really it’s built to help you save long term. How? Patience, little Timmy, first let’s pin down what an RRSP really is…

What the heck is an RRSP?

A few years ago if someone had asked me what an RRSP was I would have had no real answer for them, but in my head… I would have thought of it as some kind of ‘thing’ that you invest in.

“I’ve got an RRSP”, people say.

They refer to it like it’s an investment all in itself. Like a railway company or a million superballs.

That’s not really how it works.

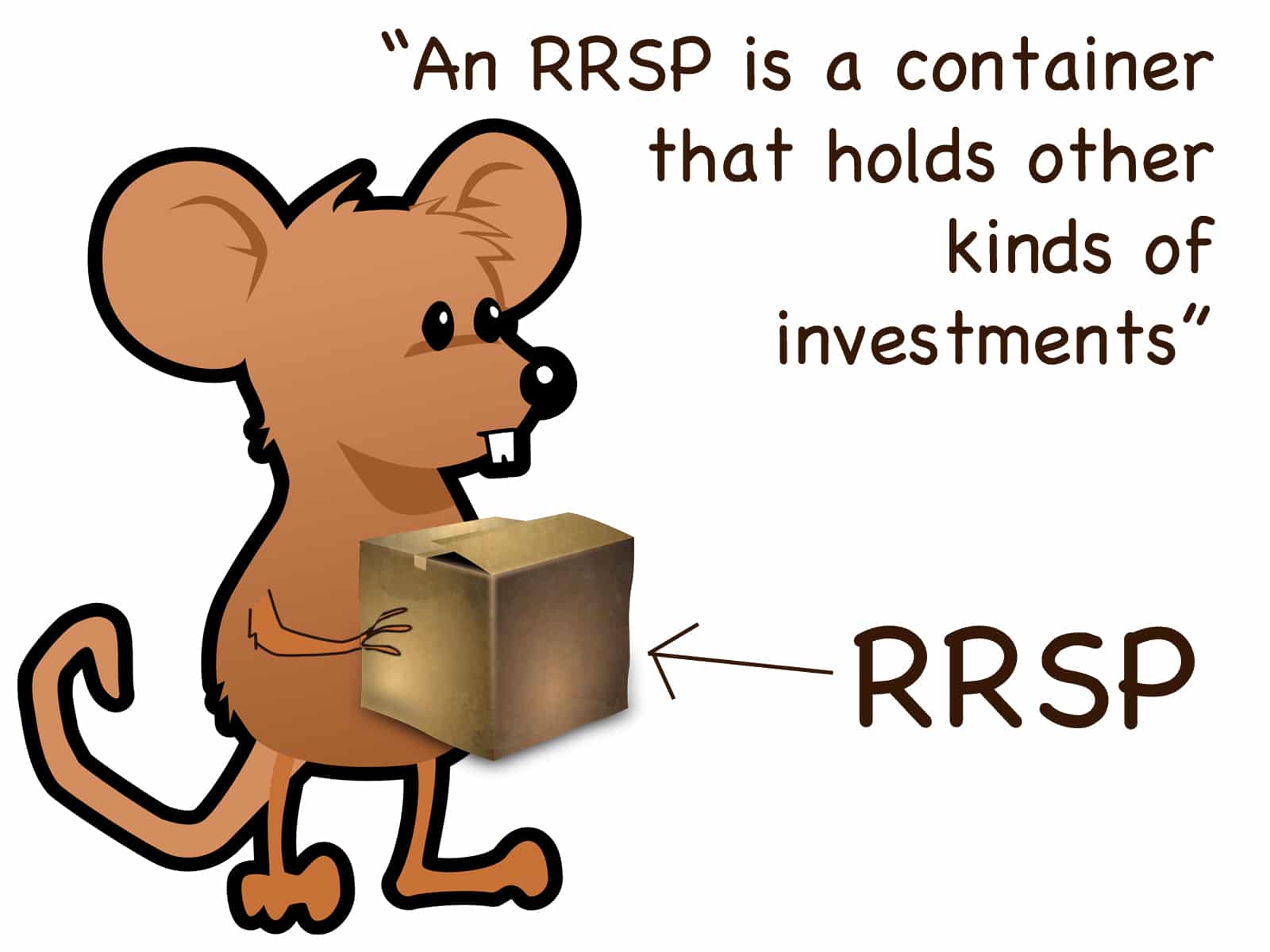

First let’s unlock those four letters. RRSP stands for Registered Retirement Savings Plan.

And what is it?

An RRSP is a container that holds other kinds of investments.

Instead of something you can actually buy, it’s more of a … box (I know you can buy boxes… just be cool).

I can put all kinds of different things in that box. I could fill it up with stocks, maybe a bond, I could put a mutual fund in there… or I could just fill it chock-a-block full of cash.

Can you put anything in an RRSP?

Can you put anything in an RRSP?

Well. No.

You can put a lot of things in your RRSP, but not everything.

And what can’t you put in?

If you’re just a regular person, there’s a really good chance you won’t accidentally put your stamp collection in your RRSP. It’s not an easy mistake to make.

Nerd fact: If you do get caught putting stuff in your RRSP that doesn’t belong there you’ll get hit with a 50% tax of the fair market value of the item in question PLUS a 100% tax on any income you made off of it. Not great.

So your RRSP is a container that holds other investments.

Cool.

How much stuff can you put in it? Is it like a Mary Poppins magic bag? Or is it like a regular old boring box..

Well, it’s somewhere in between.

How much can you put in your RRSP?

The thing that can sometimes be confusing about RRSP’s is that everyone has different amounts that they can contribute.

Why?

The official language on how it works goes like this:

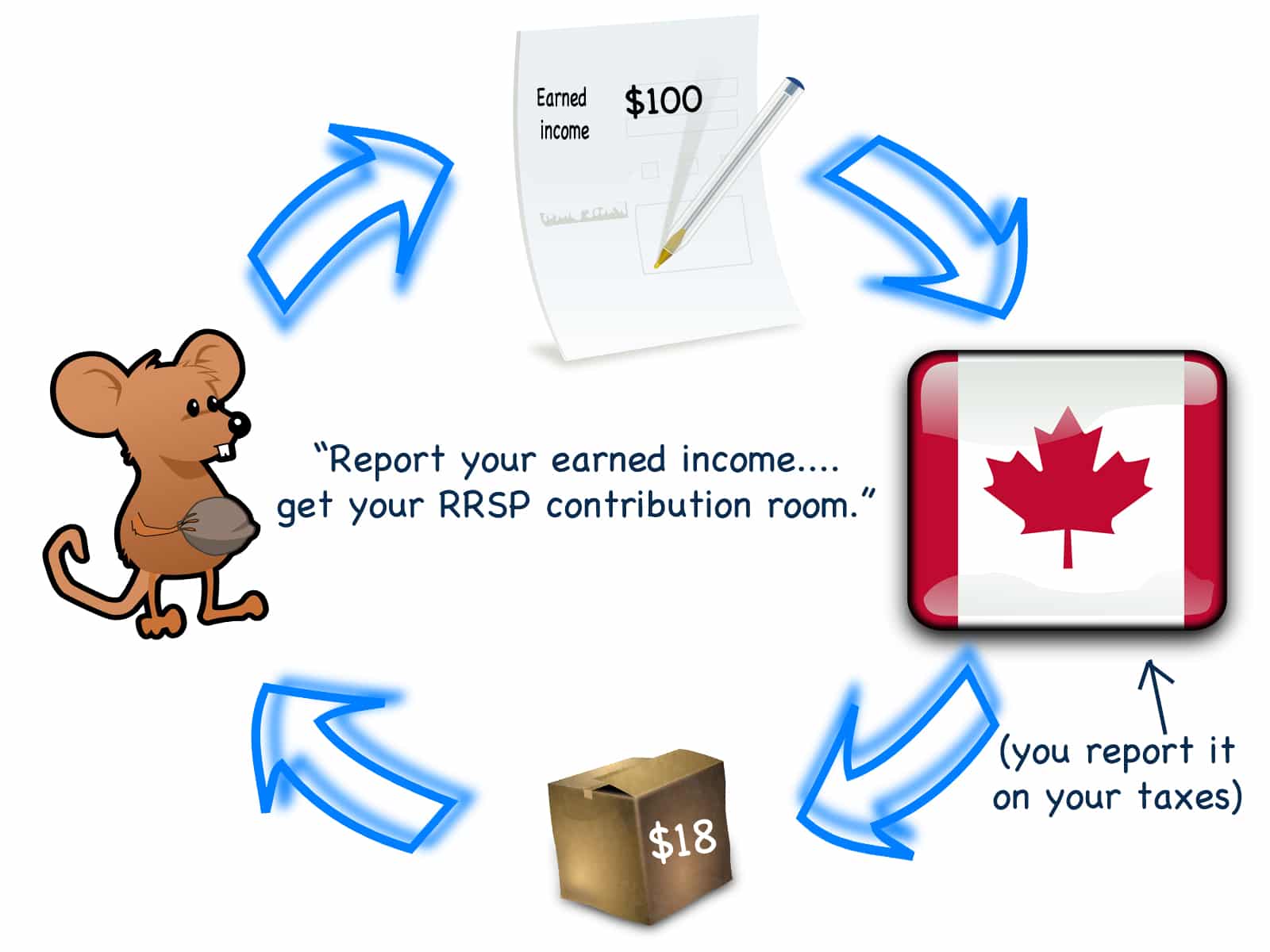

Your contribution room is equal to 18% of your previous year’s earned income to a max of $24,930.

(that’s the 2015 max)

But what does that translate to in real life?

Every year that you work (earn income) and report it to the government, the government rewards you with some contribution room in your RRSP.

RRSP PRO TIP: You can even earn contribution room as a kid! Kids won’t pay taxes if they’re only earning a few thousand dollars, but they can gain RRSP contribution room if you filed taxes for them. Fun, right? (And more proof it pays to start early!)

That contribution room is 18% of the amount you earned. If you’re earning lots of money… it all maxes out at a certain point anyways. For 2015, that point was 24,930 dollars, but it goes up a bit every year.

Every year that you earn income you get some more contribution room based on what you earned the year before.

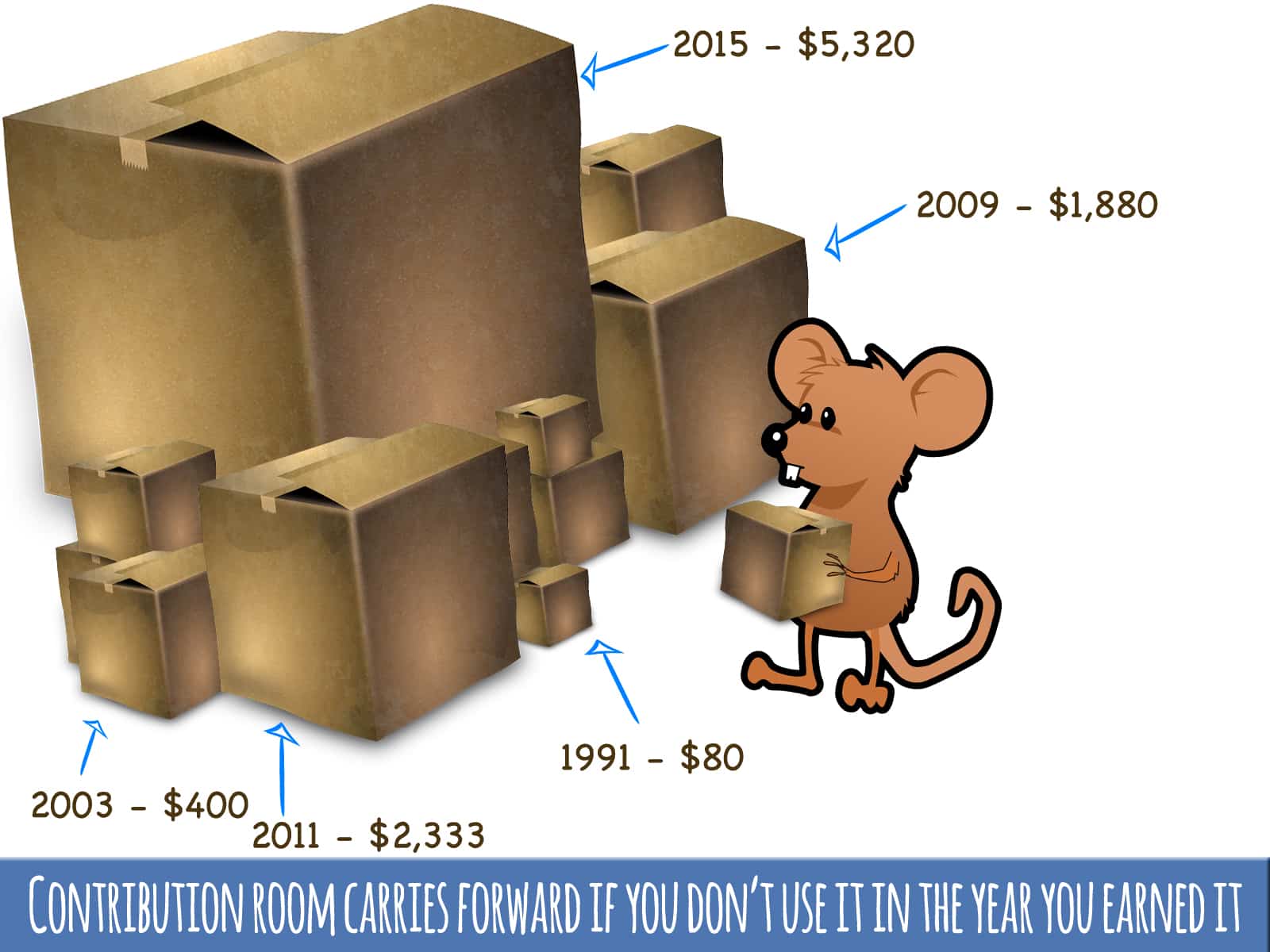

Now you may be thinking… “I don’t remember getting any contribution room. I haven’t even been using my RRSP… have I wasted it??”

Nope. Whenever you get some more room in your RRSP, you can use it at any point in the future.

So even if you can’t afford to put money away (or decide not to) you’ll have all that empty room waiting for you when you do decide to start!

A note for the regularly employed:

I know that lots of you readers are freelancer/self-employed types, but some of you are employed and maybe even have a pension!

That’s awesome. Pensions are great.

But it’s important to note that pensions change your contribution room. Basically, you have to take the amount that you/your boss put into your pension and subtract that off of your contribution room.

I know it seems unfair, but since they’re both for retirement it all evens out in the end.

Why your RRSP is straight up magic

So it’s a container. Who cares? You can put the same stuff into a normal account with your bank.

The true power of an RRSP is all about taxes.

Normally, any money you make in a year is taxed by the ole government. Depending on how much you’re making, those rates will vary… but it’s all taxed.

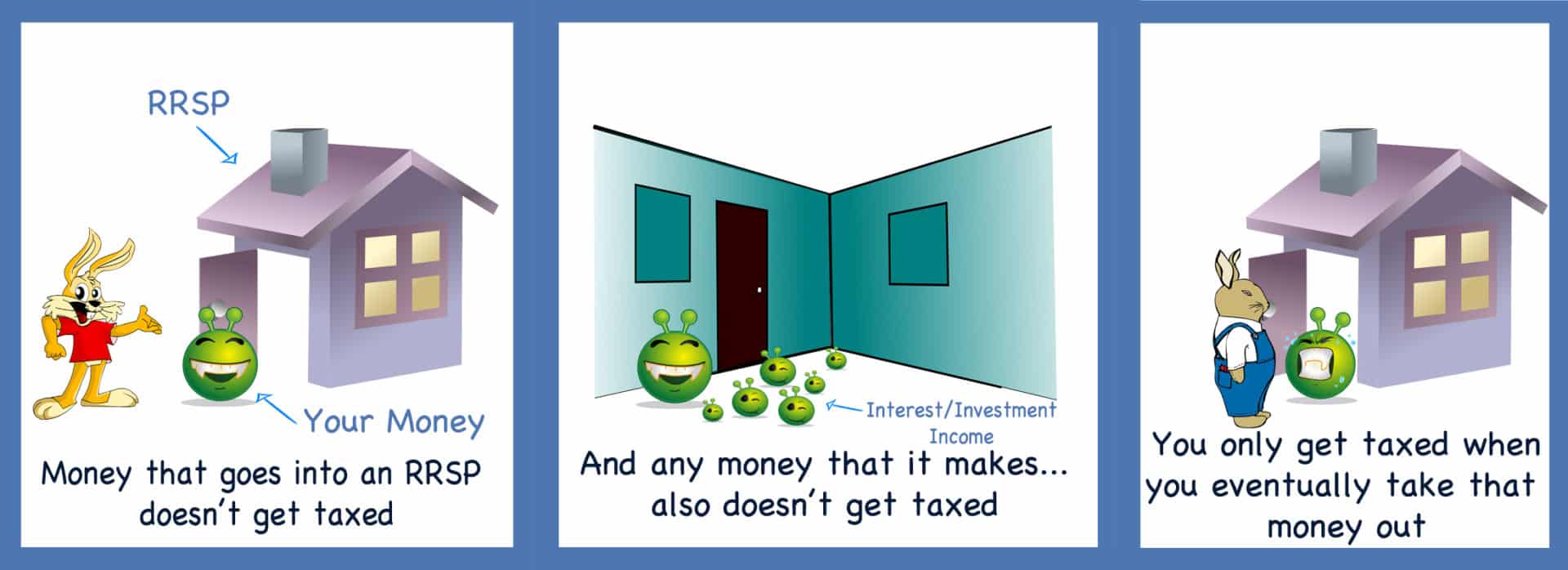

HOWEVER… if you put that money into an RRSP… it’s NOT taxed (at least not right away).

Money that you put into an RRSP isn’t taxed until you take it out… which, if you’re young (I’m calling under 40 young 🙂 ) won’t be for a loong time.

Not only will that money not be taxed right away, but none of the money you earn on it (with interest, or investment income) gets taxed until you take it out either.

Because here’s the magical truth…. There may be a limit to how much you can contribute to an RRSP, but there’s no limit to how much it can hold! So… if you’ve got stocks that are gaining value over 40 years… all that value doesn’t get taxed until the day you withdraw it!

Why the ability to delay paying tax is so awesome…

No one wants to pay taxes. So the idea that you can put off that burden on a part of your money for a few decades… sounds pretty cool.

But you do have to pay tax eventually… so is it actually that awesome?

YES. OHHH…. SO MUCH YES.

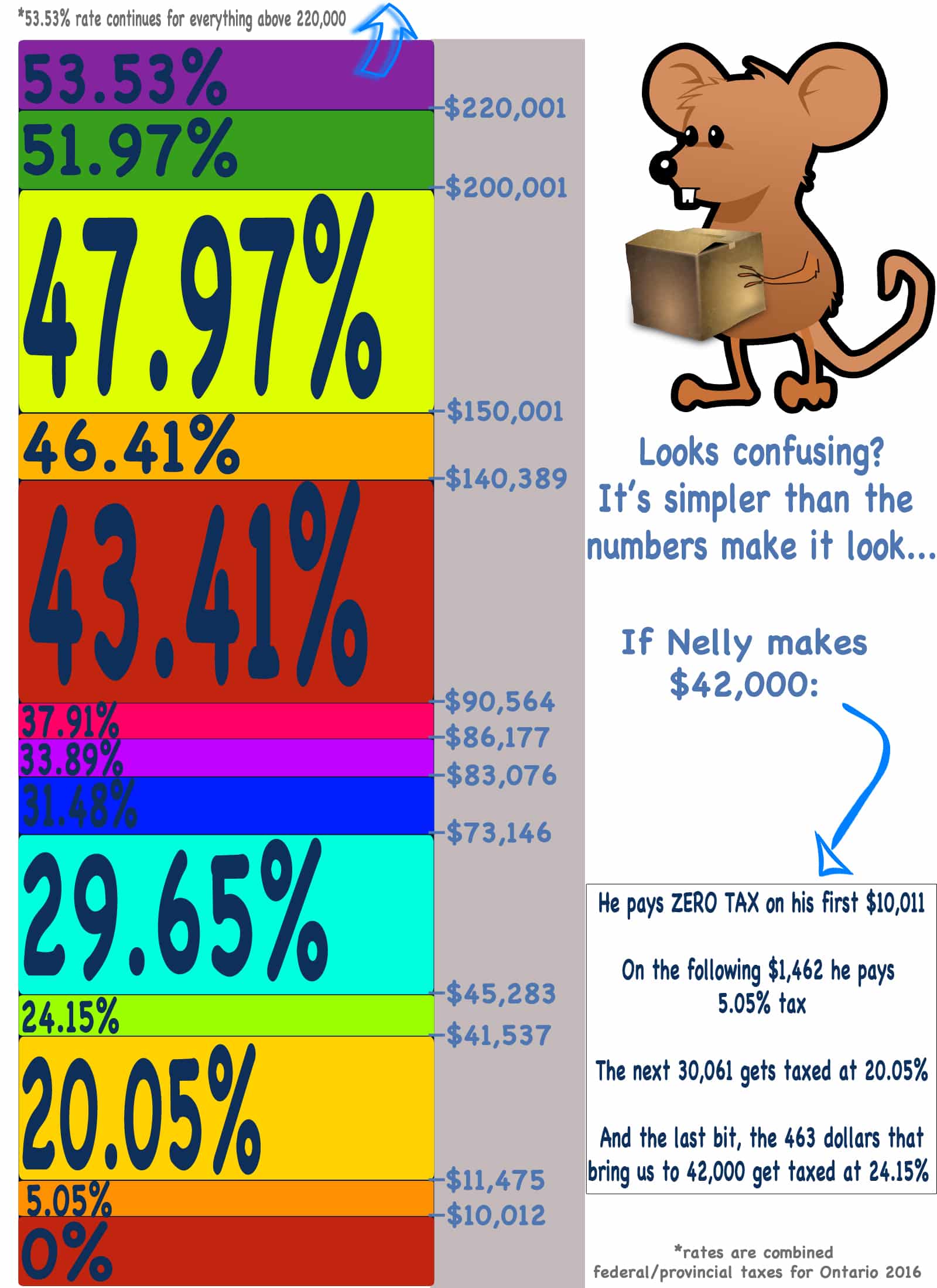

The reason comes from going one level deeper in how taxes work. Let’s get a little refresher on the magic of tax margins (I am officially overusing the word ‘magic’ in this post….#notsorry):

As you can see, you pay different amounts of tax depending how much income you’re making, but it’s not you who moves up and down the tax margins… it’s the dollars you earn.

Every dollar is taxed separately, and when you breach into a new margin, that next dollar is taxed at the higher rate.

TAX MARGINS DON’T MAKE SENSE YET? CHECK OUT THIS ARTICLE!

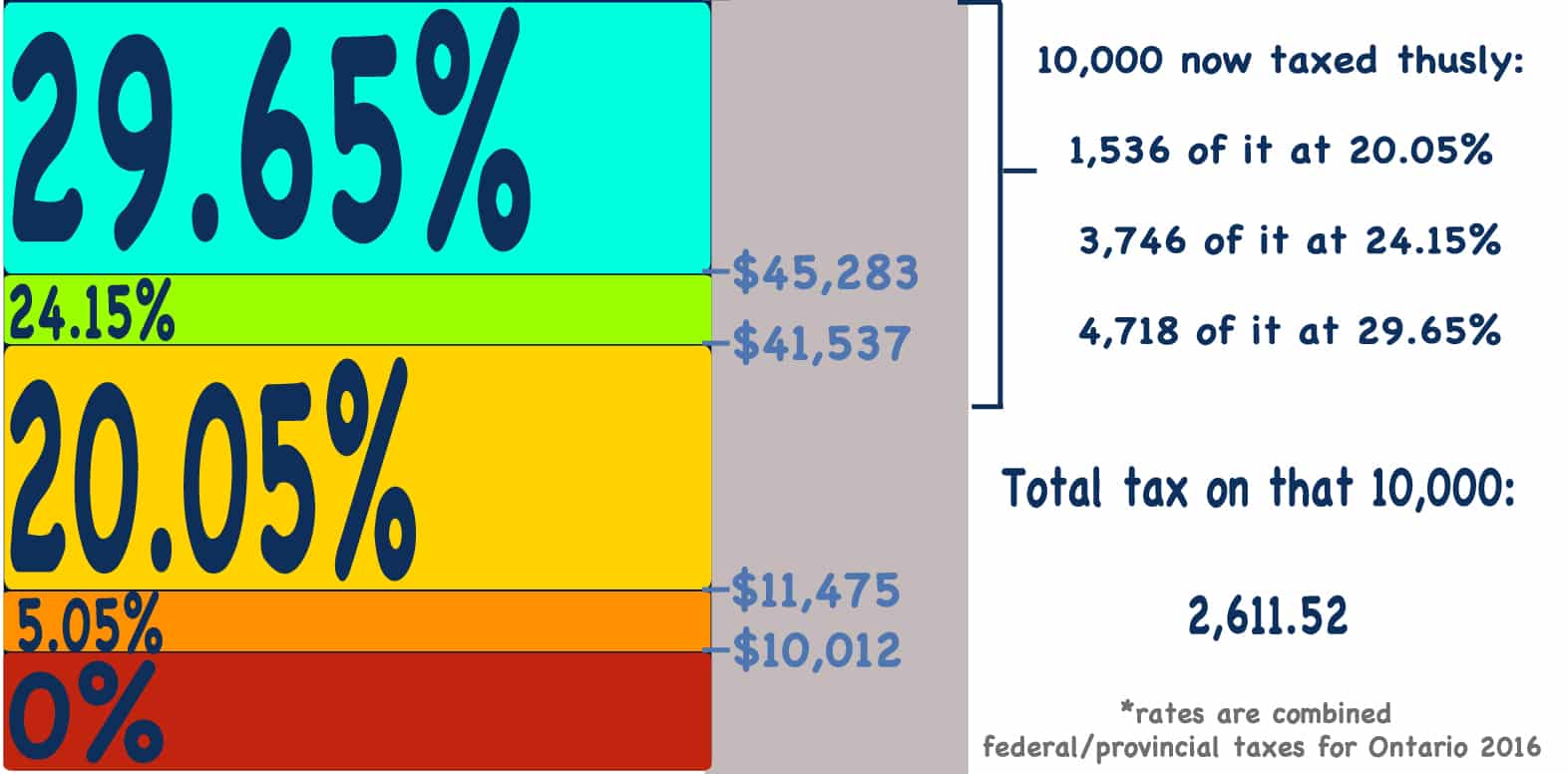

So why does this matter? OK, let’s say you make 100,000 dollars a year:

Now… if you put 10,000 dollars into your RRSP, what happens?

Well, right away you’ve decreased your ‘taxable income’ to 90,000.. which is nice, not only because you have less income that will be taxed, but because that top 10,000 dollars was mostly being taxed at 43%. That means you would have been paying about 4,300 dollars JUST on that money you socked away in your RRSP.

That’s a great saving… but it’s not completely real. At some point you will have to face the tax dragon.

The thing is… when you get to your later years, and you’re thinking about taking money out of your RRSP… maybe you’re not making 100,000 dollars a year. Heck, maybe you don’t need nearly that much. Your life might be a little simpler. Your house is paid off. The kids have moved out. Your business doesn’t need all that investment anymore.

Maybe you just need 40,000 to come out of your RRSP to pay your expenses that year.

So when you eventually take out that 10,000 dollars it’s no longer the top 10,000 of a 100,000 dollar income. It’s the top 10,000 of a 40,000 dollar income.

That money is now taxed in a way lower bracket.

You managed to save yourself more than $1,600 in taxes, just by stowing away money when you were in a high bracket, and paying taxes later… when you were in a lower bracket!

How FREAKING COOL IS THAT?? Turns out sometimes it pays to put things off…

What are the rules on when I can take my money OUT of an RRSP?

You can take your money out of an RRSP anytime.

If you want to take it out early (not in retirement) it’s not quite as easy as taking it out of a normal savings account, but you can do it.

You’ll have to sign a form/letter, and you might have to pay some fees depending on where your RRSP is.

The big disadvantage is that it counts as income for that year.

Remember, you didn’t pay tax on that money when you put it in, so now you have to pay taxes on it AND (just to make sure that you don’t take the money and run/not have enough to pay taxes on it when the time comes….), there’s usually a big ole withholding tax… up to 30%.

Not the best way to get ‘fast cash’.

Of course this all changes if you use an RRSP like it’s meant to be used, later in life, when you’re not making very much income. That process is very different … and one I’ll explain in another article (but if you want to know right now… read about it HERE).

The point is, you CAN withdraw it at anytime, but it’s not the best plan. RRSP’s are for the long term.

There are two exceptions to the early withdrawal penalties, the Home Buyers Plan, and the Lifelong Learning Plan…. Both of which we’ll discuss in another RRSP deep dive (I promise it will come soon)!

When is an RRSP the right tool?

An RRSP is undeniably an awesome tool, but like any tool… it’s not useful for everyone, in every situation.

An RRSP is definitely at its most effective if you’re in a high tax bracket when the money goes into the RRSP, and a lower bracket when it comes out.

That’s when you’re taking full advantage of putting off taxes to another day.

An RRSP can be not so great if you’re making very little money (in a low tax bracket) when you put it in, and making more (in a high tax bracket) when it comes out. You’re actually paying MORE tax in that situation.

But practically speaking, an RRSP is also a really really useful forced savings tool.

I know lots of people who use it mainly because it’s really hard to withdraw money from. It’s not built to be a regular savings account, it’s built to save for the long haul… so if you’re a person who has a hard time not dipping their hand in the cookie jar (the cookie jar is your savings)… an RRSP can help you stay away, no matter what your tax rate is.

Why I stopped using mine…

I stopped contributing to my RRSP after I learned how this all works.

Not because I had turned my back on the idea of long term savings, but because I realized it wasn’t the right tool for me.

I generally hang out in the lower tax brackets #moneybags.

So no matter what happens in my future… I can be pretty positive that I won’t be taxed at a lower rate at that time than I am now.

That’s why I made a different choice for my long term savings.

I take those hard earned dollars and throw them into another 4 lettered financial acronym: the TFSA.

Why? Well… you’re going to have to wait and see … because this piece is already epically long and you need a break.

Go and drink a beer, but be sure to stay tuned for Part 2: RRSP the deep dive continues (how to use an RRSP to buy a house and fund an education), AND the dramatic conclusion: TFSA’s – the myth, the truth, and more pictures of a really cute mouse trying to get control over his finances.

What about you guys? Do you use RRSP’s or just ignore them? Why do you love/hate them?

I used to contribute to my RRSP and use the tax refund to buy down the mortgage. Then decided it would be better to use the money to just buy down the mortgage, skip the RRSP. Would like to hear your thoughts on that.

Strategic financial planning Sydney is crucial for your future. Focused Advice can help you review your cash flow and create a road map that you can follow.

http://focusedadvice.com.au/services/financial-planning/

Credit Fix Solutions Australia

http://creditfixsolutions.com.au

Sydney Aged Care Financial Advisers |

http://www.sydneyagedcarefinancialadvisers.com.au/

Reverse Mortgage Lender Australia, Heartland Seniors Finance

https://www.seniorsfinance.com.au/