*I am not a tax professional. This is meant to be an educational tool and NOT a recommendation. Each personal situation is different and there’s a lot of grey area in self-employed deductions. If you have questions (even just little ones) … talk to a tax expert.*

If you’ve been keeping up with the blog over the last year you’ll know that I spent insane amounts of money on my teeth in 2015.

In fact, it was my biggest non-business expense (more than my housing costs).

And yes… that was after dental insurance, of which I have a minimal amount. #humblebrag

So, now that it’s tax time I found a way to turn some of that excessive spending into a tax credit!

YAYYY!!!

… and it’s not just for dental, it’s for a whole bunch of medical expenses!

What is the Medical Expense Credit?

It’s a non-refundable tax credit for people who have had significant medical expenses. For single folks … they can just use their own medical expenses, but if you have dependants (a spouse or kids) you can claim their medical expenses, too!

This credit only pays off if you have quite a bit to claim. If you’ve only got a few hundred dollars of expenses… it probably won’t be worth it.

Remember that this is a CREDIT, not a deduction. That means that it gets applied directly to the taxes that you owe…

Need a brush up on Tax Credits? Check this out!

What qualifies as a ‘medical expense’?

- medical and dental services

- nursing home care services at home or in an institution

- ambulance services

- glasses/dentures/hearing aids

- prescription drugs

For a full list of things that qualify go HERE.

How does claiming the credit work?

Here are a few things you need to know if you want to claim this credit:

- You need receipts. (#taxfact)

- You can claim expenses in a 12 month period (it doesn’t have to be the calendar year)… so pick the 12 months that are most advantageous, as long as they end in the current tax year – if you’re confused about that… talk to an accountant.

- There’s no maximum to how big this credit can be (isn’t that nice).

- You can’t claim an expense that was reimbursed. If an insurance company paid you for it already… don’t claim it.

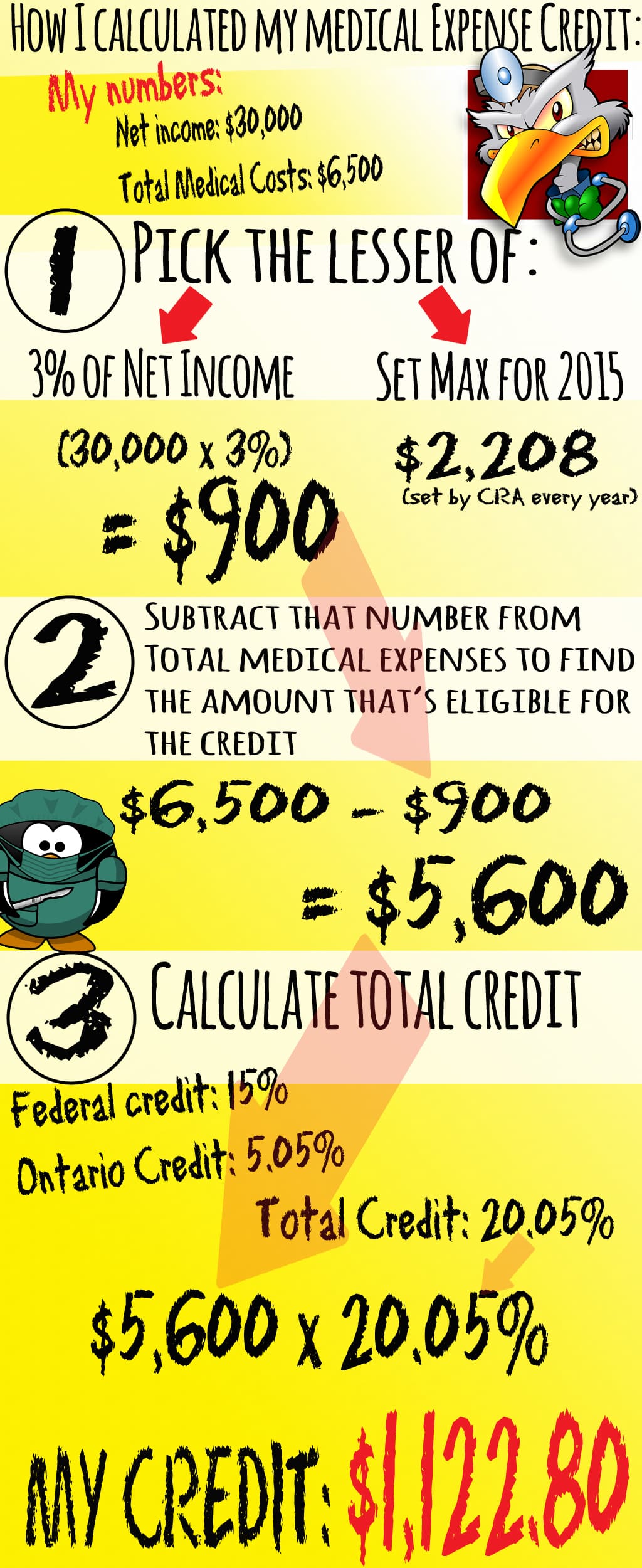

How much do you get?

I told you that this credit is really only good for substantial amounts. So when you’re calculating you have to look at a few numbers:

- What are your total medical expenses?

- What is 3% of your NET income (that’s income after all the deductions)?

- $2,208 (the set max for the 2015 credit)

Got those?

Okay… so now take a look at your #2 and #3 numbers

Take the lowest one.

Subtract that amount from your total medical expense!

The rest of that amount is eligible for the tax credit. If you don’t have an amount left… this credit probably isn’t for you.

The remaining amount gets a 15% federal credit AND a provincial credit (Ontario is 5.05%).

How I found my total medical (read: dental) expense credit:

I don’t have my exact numbers (I’ll be going through that later today), but I’ll give you some general ones so that you can understand how it works.

Err, your glossary says that tax credits are “infinitely more powerful” than deductions, but it depends on how you frame it. For most people an expense that’s counted as a deduction is worth more than one counted as a credit because they compare to the size of the expense. For instance, the medical expenses here: $5600 in medical expenses creates a credit of $1148. But if you could deduct the medical expenses ($6500 less the “suck it up” amount that depends on income) then it would be worth at least $1148 and as much as $2100, whereas as a credit it’s a flat value (actually decreasing as your income increases and the “suck it up amount” increases).

A $5600 credit would be worth more than a $5600 expense deduction, but that’s not really an apples-to-apples comparison — if I had a $5600 expense I would prefer that it was counted as a deduction.

An important thing to add to the list of things that count as a medical expense is insurance premiums for private health plans (though not if you’ve already deducted those as a freelancer business expense). Plus some weirdo things like the incremental cost of gluten-free food (but only if you actually have celiac disease and not because you’re being trendy).

Wayfare and I really need to get our glasses schedule in sync — we keep buying them in alternating years instead of both buying a pair in the same year, which would go a long way to putting us above the suck it up threshold.

That’s a really good point. It’s so easy to fall into the trap of looking at taxes only through your own personal lens…

In this case you’re completely right, a deduction might be a ton more valuable than the credit. Although I’m still pretty grateful for the credit … since a deduction isn’t on the table.

As for the other things that you can count towards your medical expense… there’s a bunch. I didn’t know about the incremental cost of gluten-free food… that’s kind of awesome. Is that actually on the CRA site, or is that something you’ve puzzled out through your own research? How do you determine the cost difference between shopping gluten free and ‘normally’?

The gluten-free thing is actually on their site — the link you have above for the full list, section 1.136. They have an example of finding the incremental cost here: http://www.cra-arc.gc.ca/tx/ndvdls/tpcs/ncm-tx/rtrn/cmpltng/ddctns/lns300-350/330-331/clc-eng.html