Investing. The holy grail of financial wizardry. You put money in, you get more money out. Whether it excites you or it scares you it can be a little tough to understand the intricacies of the whole investment world. But there’s one great investment that a lot of people are sitting on that is 100 PERCENT GUARANTEED.

Your debt.

These days, most people seem to have some kind of debt… whether it’s the kind of debt that’s okay to talk about: mortgage/student loans, or the kind that we secretly stress about at 3 in the morning: credit cards, tax debt, and the money you owe Vinny the loan shark.

There are lots of reasons to take care of your debt. For me, stress was a huge factor, but that’s not true for everyone. So if you need a push, or a new reason to take another look at aggressively paying off your debt… try this one on for size:

Paying off your debt just may be the best guaranteed investment you can make right now.

There’s a term that people kick around when talking about investments: Return on Investment (ROI.. If you wanna be financially fancy). It boils down to the amount you get back from investing money into something. If you buy a stock, the amount that its value goes up in a year is your ROI. If your house value goes up…. Hey, presto… a return on investment.

But as with most things that you invest in, there’s an element of risk. Prices can go up, but they can also go down (I know… mind blowing). There’s no real guarantee of a return on your investment.

And this is where your debt comes out on top.

Every month, you pay someone for the privilege of holding on to your debt, whether it’s the government (student and tax debt), or the bank (credit lines, and cards). The fee you pay for that privilege is your interest rate… and it can get pretty scary over a long period of time.

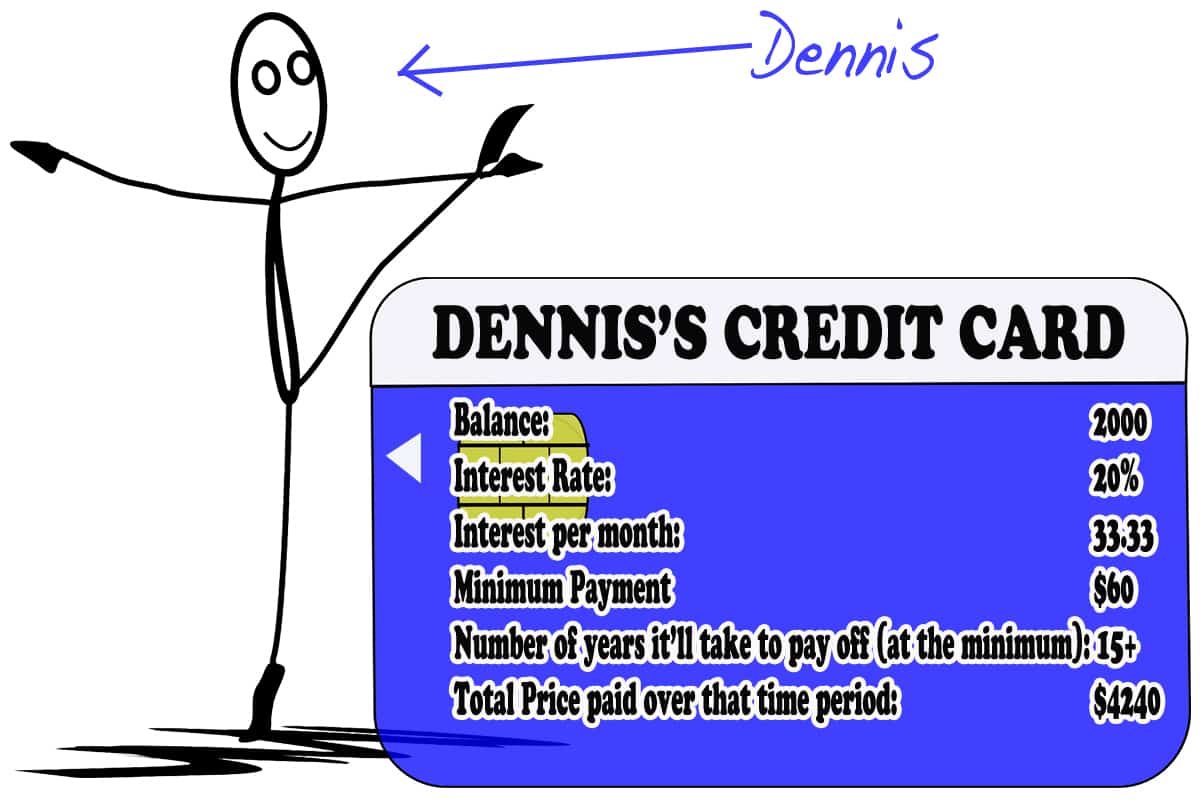

Let me paint you a word picture:

Meet Dennis: he’s just a normal artistic dude, with a little normal credit card debt.

These numbers are based on the assumption that Dennis stops using his credit card, and only pays the minimum payments every month.

This isn’t a post about how you should pay your credit card faster because it’s costing you a ton of money (or any debt really… credit cards are just the most dramatic example). This is a post about how you should pay down your debt, because it’s the BEST POSSIBLE INVESTMENT FOR YOUR MONEY.

Putting more than the minimum payment towards the balance doesn’t really feel worth it to Dennis. He feels like it’s sucking up money that he could be using to actually invest - in his career, the stock market, or one of those fancy GICs everyone’s talking about.

Dennis might feel like he has a black hole on his hands. But what he actually has in that credit card debt is an investment, with a guaranteed return much higher than any of those other options.

I promise you that if the banks found some way to offer people a GUARANTEED 20% RETURN ON INVESTMENT that Dennis would be losing his freakin’ mind.

It’s important to remember that your finances aren’t just measured by how much money you have in your bank account. It’s a bit more big picture than that. It’s about your net worth (which is basically just your assets minus your debts). So whether you’re increasing your assets, or decreasing your debt… the results are the same…. You, getting into a better financial place.

Right now the money sitting in your savings account is earning just over ONE PERCENT interest. BLERG. And even if you’re in the stock market (which is doing quite well right now… unless you’re invested in Canadian oil fields… then… less well) the returns are probably less AND they’re not a sure thing.

Paying off your debt is a lot less sexy of an investment than buying property, or building a stock portfolio, but it’s really simple, is hugely beneficial, and (in case I haven’t made it 1000% clear) it’s totally guaranteed.

So pay off your debt with pride, and next time the topic of money comes up while you’re sitting around the family dinner table, or at the bar… slip in to the conversation that you got a sweet tip on a guaranteed investment that’s paying you 20% a year (or whatever the percentage on your debt may be). And as your friends and family try to tear the secret out of you, sit back and sip your drink like the financially savvy wizard you are.

Silly muggles… they’ll never learn.

Want to pay off your debt... but can't quite seem to get to the 'doing it' stage?

Why not try out this workbook?

It'll help you get organized, and it only costs 8 bucks.

Want to start getting control of your money? How can I help?

Chris Enns

Financial Planner/Opera Singer

Money never came naturally to me. In fact... I was a bit of a disaster. I remember (very clearly) what it feels like to be 'financially out of control'.

And honestly, I still get stressed about money... that doesn't stop... the difference is that now I have the tools to deal with that stress.

And those tools are what's made it possible for me to build a life full of the things I want: art, creativity, travel, family and more.

If you want to start getting control of your money I'd love to help. You can start with THIS QUIZ, visiting my GETTING STARTED PAGE by checking out my SERVICES page.

Almost every game developed for the PC has been largely linked with fast-paced action, violence and aggressive conduct.

Not too long ago television and video games were more beneficial.

When you sit and do the same thing again and again, muscles

wear out.

This is an extreme example of high-interest debt that nobody should be carrying in the first place.

If you look at average mortgage rate of 2.5% or less, then investing in relatively low-risk mutual funds like index funds would make a lot more sense.

You’re totally right. It is an extreme example, but tons of people carry credit card debt.

The mental side of debt is a tough thing, so flipping the script and thinking of it as a great investment can help break the cycle of avoidance.

Of course, as you said, when you start looking at lower rates and comparing them to historic returns on more conventional investments the answers are much murkier (and different from person to person)

Thanks for the comment!

The math is also fairly simple. Lets say you are in a 50% tax bracket to make it easy.

That means you need to make $2 to keep $1. If you are paying off the debt with after tax dollars then in effect you would need to get double the return on your money. In order to get back the dollar you paid in taxes you need to get 100% on your after tax dollar. So if you are in a 50% tax bracket you need to double the interest rate you are paying on the debt in order to figure out whether it makes more sense to invest or pay down debt. If the interest rate on the debt is 2.5% then you just need to get more than 5.00% on your investments for it to make more sense to invest. That is assuming that you invest in a GIC whose interest is fully taxable.

So in your example the 20% interest rate would be the same as receiving 40% return. So it makes more sense to pay down the debt in this case.

The math may be simple, but everyone’s personal situation sure isn’t.

You’re totally right in what you’re saying, but it sure goes to show that there are so many things to consider when trying to decide where the best place to put your money is.

Debt vs Investment isn’t a cut and dry issue, but I think (especially for investors with less experience) it can be a good place to look first.

Thanks so much for the comment.

Good blog, but there is a critical point that was missed that makes paying off debt even more attractive; it is an after-tax return. If you are in a 40% tax bracket and have savings in a non-registered account, you’d need a 5.83% return, guaranteed, to equal what you’d “earn” by paying off a 3.5% mortgage. Try sitting around a dinner table and telling everyone you’ve got a guaranteed investment that pays more than 5.8% every year, compounded, (that’s the equivalent of a 3.5% mortgage). You won’t find a GIC anywhere near that amount.

Totally true. Thanks for the comment.

Paying off high interest rate debt is certainly the way to go. However if you are paying 2.5% on a mortgage and can make more than that on a balanced investment portfolio I don’t think your argument is very strong. You would be better off paying down your mortgage over less than 25 years so reduce your amortization and investing whatever you can into a TFSA or RRSP.

Though I have peers who are opting to both save for retirement/vacation/whatever and pay off debt we are choosing to put 100% of our money towards our debt. I love the 100%ROI and quite frankly it makes me feel great to see the balance go down.

I totally agree. There’s nothing wrong with spreading the money around, but the thing is… when you think about it in terms of net worth it’s all the same… add to the positive side, or subtract from the negative…

The only difference is that debt tends to get worse if left alone. A little extra incentive to put it at the top of the pile.

Like The Roamer, I, too, can’t believe this didn’t click for me.

Thanks for sharing this great tip!

Its so amazing how this doesn’t click until someone tells you.

I didn’t think about this until I read a similar article by MMM. But it was an ah ha moment for sure.

Also I think its perfect how you dropped in the word muggles. . (harry Potter fan over here)

Thanks Roamer… I do like a good harry potter reference…

I figure… enough of the shame of debt. It happens… you might as well see it as a glass half full opportunity.