I had a lovely weekend.

It was one of those rare weekends when you close the computer, set the smartphone aside and have wonderful quality time with the people you love.

I won’t bore you with the details, but it was capped off by a great day of diner brunch and walking through the neighbourhood with my girlfriend, and after 3 coffee stops and the discovery of a new secret perogie den we walked into our first open house.

I’m sure you’ve done it.

It was in our neighbourhood, and we were curious.

We’re not actively looking for a home, but we’ve definitely played around in the insanity of the Toronto mortgage market (if you want to read that whole sage check out THE MORTGAGE FILES, it's in 7 parts, and it's ridiculous).

So we walked into the house, and it was exactly what you’d expect.

Newly renovated. Shiny new kitchen. Everything white. Nicely staged.

It looked exactly like all the houses on the reno shows.

And I didn’t want it at all. It was interesting to see, and it even had a legal basement apartment (which is rare in Toronto… not the basement apartment part, but the ‘legal’ part).

But we left, and I was fully righteous in my “I don’t have the urge at all to buy something like that” feelings. Which led to even more self-righteous “prices are crazy, who can afford these things” conversations.

Oh. The house that we saw was listed at $980,000.

It was “way too expensive” I said. It just “wasn’t worth it” I said.

And so we kept walking. And I kept railing on about real estate, and its role in a balanced investing portfolio... all the things that I picked up from reading PF blogs, and through my coursework.

All the right answers.

And then we saw it.

Another open house.

This one was huge. A detached brick house in a great neighbourhood.

“How much do you think that one's worth?” I asked my girlfriend.

“1.5” she guessed.

I guessed 1.2 (prices are in millions).

The answer was 1.7 million, and by the time we left that house I wanted it so much.

Love is blind (and also completely unaware of the consequences of a 25 year amortization)

It’s just one of those houses. Full of real character. Creaky in the right places. It was 3 stories, with so many bedrooms, and nooks, and interesting spaces. You don’t see a lot of houses like that. Amazing little details. It could be separated into two units, basement/main floor and the upper two floors, really easily. We would, of course, live on the upper two levels (because this was clearly happening). Sure there was no kitchen there right now, but the connections existed, and we would just live with a hot plate and a bar fridge until we could put the work in.

You know those moments when you can see exactly what your life would look like?… a flash into your future. That’s what I had, sitting in those empty rooms… imagining family, great food, a full life…

And as we walked away this is how the conversation went.

“Man… that’s the kind of house I could really see us living in.”

“I know. Too bad we don’t have 1.7 million dollars.”

“Right? For another lifetime…”

“Unless….”

Was it really that unaffordable?

Honestly, when numbers get big it’s hard to tell the difference between 980,000 and 1.7 million (I know it’s actually $720,000… but the mental difference… just be cool, ok?!).

Houses in Toronto cost so much money that you become immune to the crazy prices after a while.. and so in this case we started thinking… would it really be so impossible?

"You don’t find a property that you fall in love with very often, not like this, this is special…"

It was clear (in this rational delusion) that it would be hard. But we weren’t afraid of hard work. What if we could make it work? We could scrounge together some kind of downpayment, as long as we could afford the mortgage…. AND of course we would rent out the main floor which would bring in a bunch of income.

Was it crazy?

Why it was completely crazy

Look. Deep down we knew it was crazy.

But it’s amazing how, at the same time, I think we both had built up a tiny glimmer of hope. A hope that you grow in the secret place in your heart when you find something you really really want. It has nothing to do with the financial. It has nothing to do with reality.

It’s like that feeling you get as a kid when your parents say you can’t have a dog because it’s too much work… but you know that you would do any amount of work if you could have a dog. You’d feed it. You’d walk it every day. They wouldn’t even need to worry about it… you would do EVERYTHING.

The little kid that lives in my heart felt that way about this house.

Until a mortgage calculator broke my dreams.

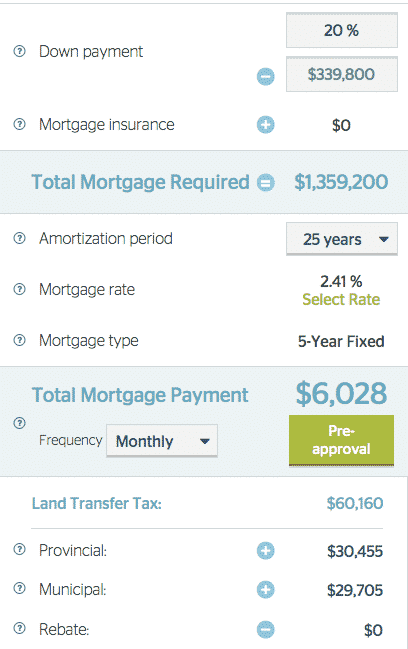

*All images come from the crazy awesome mortgage calculators at RateHub. Whether you’re buying, or just want to play with some numbers you should check them out… they’ll give you a great idea of the real cost for a home.*

First fun piece of news… no 5% downpayment on this puppy. Nope. But I could pay 20%. Which you know… is only 339,800. Easily affordable for two average people….

Why not 5%? They changed the rules! You can learn all about it here!

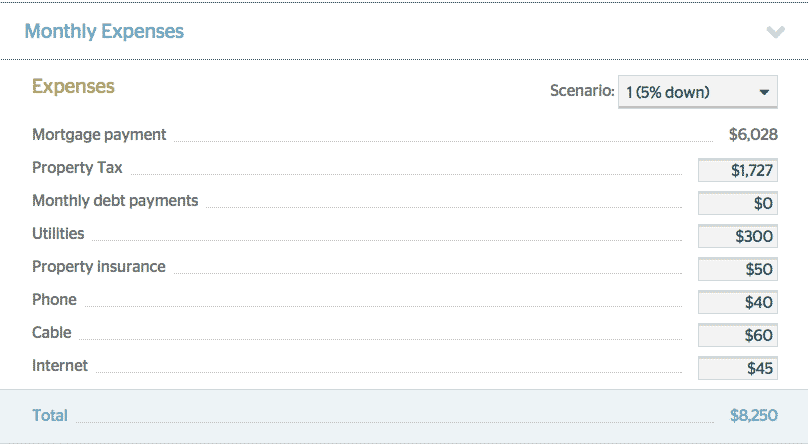

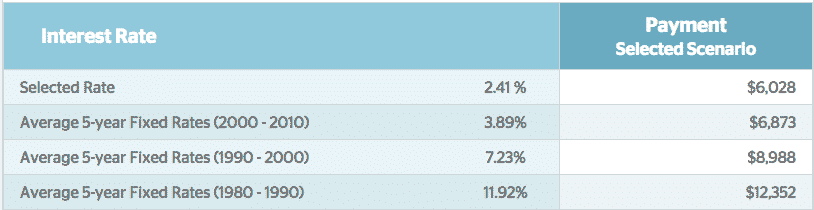

Then after choosing the lowest possible rate (that I probably wouldn’t qualify for) I ended up with the wonderful monthly mortgage payment amount of $6,028.

Okay.

After rental income, even if we gouged the crap out of our tenants, we’d be responsible for over 3000 dollars a month. Possible… maybe…

Just need to find 300,000 dollar for a downpayment…and then BAM. Land transfer tax.

I guess I need 400,000.

It was at this point that I concocted an elaborate scheme to secretly pose as our current landlord, sell the house that we’re renting now, and use the money to live the dream that I now held above any other dream.

If we could just get that downpayment… then we could maybe afford this thing.

And then RateHub smashed my dreams again… I mean… educated my dreams out of me….

Property tax. Utilities. And that’s all before some kind of emergency fund… because in a big house like this… stuff is going to go wrong.

Plus, we’re not even talking about all the money that we’d need just to make it rentable, and livable for us.

But even though the dream was dead at this point, I’ll leave this out there as well - the mortgage fee that I was dreaming about maybe possible affording (#notevenmaybe)… was the one at the crazy low interest rate that exists right now… but also might not last.

So the good folks at RateHub gave me this tasty treat... a show of what the payment would be if rate went up.

12,352, eh? A month you say?

I’m not saying that I could almost live the entire year on that.

But I could.

And I have.

5 ways to talk yourself out of buying a 1.7 million dollar house

I know you want it. I want it too.

But maybe you shouldn’t get it.

Why?

Number 1: You can’t afford the downpayment

It’s the first thing that people look at. Sometimes I feel like it’s the only thing that people look at…

The downpayment is big, but it’s also more than just the 5/10/20 percent that you’re putting on the house. There are closing costs, and land transfer tax. There’s the cost of renovating, and the costs of setting up an emergency fund.

You’ll probably need a lot more than you think you do. Talk to people who have bought, ask them what the surprises were, and plan ahead.

Don’t just talk to the bank.

Banks are made up of a whole bunch of nice folks, but they don’t always have your best interests in mind. Find someone you trust, and ask a whole lot of questions so you know exactly how much you need to have up front.

Number 2: You can’t afford the monthly payment

When you go to a regular mortgage calculator and type in your downpayment and the cost of the house… it spits out a monthly payment.

And it might look super affordable.

But usually it’s leaving a whole bunch of things out.

The monthly cost of a home is so much more than just a mortgage payment. It’s insurance, and maintenance, and utilities. RateHub's calculators can give you a better idea of what to expect, but here’s another situation in which talking to people who own houses can be a great idea.

It doesn’t matter if you can afford the downpayment. It’s the monthly payment that you have to worry about… for the next 25 years.

Make sure you can afford it. And make sure you can afford it with wiggle room, because like we talked about above… interest rates can change…

Number 3: You don’t want your entire savings sunk into one thing

When smart people talk about investing they talk a lot about ‘diversity’.

Basically, it boils down to… if you have all your money in one kind of thing, and that thing loses value… all your money is gone. BUT if you have your money spread around in a few areas, then even if one is doing badly the other ones might be doing okay.

Putting all your money in one kind of investment, like a house… is risky.

I know lots of people (boomers) like to talk about how their house was the best investment they ever made, and that’s great for them. A lot of people bought cheap houses, and they gained a lot of value. But that doesn’t mean it’s right for you.

Having all your money in one kind of asset is a big risk. It might pay off, it might not pay off.

Do you want to take that risk?

Number 4: You don’t want to lose the flexibility

If you’re really rich, you don’t have to worry about flexibility, but if you’re really rich, why are you reading this article?… not a judgement, just a question.

For the rest of us, we need to think about the fact that even if you can afford the downpayment, and the monthly payment, and want to take on the risk…. there’s a good chance that this house is going to take a huge percentage of your resources to maintain.

Time and money.

It’s like when you’re a kid and you want something really big for your birthday, and your parents say that it’s too much… but you say it will count as your next 5 birthdays, and Christmas presents.

It’s great when you get that big present, but come Christmas.. It kind of sucks. And then the next Christmas … it’s worse.

Are you willing to give up the other luxuries that money/time could go to? Things like vacations. Fun toys. Or just the peace of mind that having some extra cash sitting around gives you.

When you take on a huge asset, like a wonderful house, you’re probably going to take a hit in the flexibility department.

Something they talk about a lot in investing is opportunity cost. Whenever you invest in something, you lose the opportunity to spend that money on something else. What you need to figure out is whether the loss of that opportunity is worth it.

Is it?

Number 5: You don’t want to worry about all the things that could go wrong

The bigger the house, the more things that can go wrong. People don’t talk about their big old houses as money pits because it’s a romantic turn of phrase…

They really can be.

If reno shows have taught us anything it’s that nightmares live behind the walls: electrical problems, plumbing problems, mold problems.

Owning a giant asset like a giant house can be really stressful, and it’s not for everyone.

I know we like to talk about home ownership like it’s everyone’s dream, but I really don’t think it is. More and more people are renting. More and more people are finding other ways to spend and invest their money.

Sometimes it’s about a better return on investment, and sometimes it’s because the idea of homeownership just isn’t worth the trouble.

I rent, and when something goes wrong… I send an email to my landlord.

Which is pretty awesome.

Does the idea of being on the hook for everything that could go wrong stress you out, or fill you with the excitement and gravitas of a young elk?

Should you buy a big, expensive, beautiful house?

I don’t know.

I shouldn’t. That’s abundantly clear.

At least not right now.

There are so many opinions out there on what you should be doing with your money. I tell you, if I had the money for a house like that, and the income to support it… man … it would be a tough call.

Because I really loved it.

And that’s a great reason to buy a home. Except also… I couldn’t afford the downpayment, or the monthly costs, nor was I willing to take on the risk, and I love my flexibility…

So turns out, for me, this was more of a ‘catch and release’ situation…

What about you? How do you talk yourself out of making crazy, insane financial decisions? Would you try to buy it (if you had the money)? Remember… it’s super beautiful…. 🙂

Want to start getting control of your money? How can I help?

Chris Enns

Financial Planner/Opera Singer

Money never came naturally to me. In fact... I was a bit of a disaster. I remember (very clearly) what it feels like to be 'financially out of control'.

And honestly, I still get stressed about money... that doesn't stop... the difference is that now I have the tools to deal with that stress.

And those tools are what's made it possible for me to build a life full of the things I want: art, creativity, travel, family and more.

If you want to start getting control of your money I'd love to help. You can start with THIS QUIZ, visiting my GETTING STARTED PAGE or by checking out my SERVICES page.